.png)

.png)

Stocks rebounded strongly last Friday, recovering the ground lost during the week, as Treasury yields stabilized. Friday's rally came a day after Federal Reserve Chairman Jerome Powell said at an International Monetary Fund conference that the Fed would not hesitate to tighten monetary policy if the data supported a hike. While markets are pricing in less than a 20% probability of a December rate increase, a stronger-than-expected CPI report or hot retail sales print could reset expectations. However, investors jumped back in, reclaiming the notion that U.S. rates have peaked which had sparked the rally in risky assets that had extended through eight straight sessions until Thursday.

Stocks had a big rally day on Friday, but most of the week was a real struggle. The rally on Friday didn't help the equal-weight SP 500 or Russell 2000 finish positive for the week, despite the SP 500 and the Nasdaq 100 finishing higher by more than 1 and 2%, respectively. It appears to be more of the same, with just a handful of stocks continuing to power the major indexes higher while the rest of the market is left behind.

Oil prices fell for the third week in a row to the lowest level since mid-July as mixed data on the global economy raised concerns about demand for oil. On Friday, U.S. crude was trading for around $77 per barrel, down from about $89 three weeks earlier.

Late Friday with the market already closed, Moody's Put the US credit rating on negative watch, which puts the US one step closer to a credit rating downgrade, which is a pretty big deal and could mean that bond yields start moving higher again.

OPEX and U.S. CPI will drive trading in what could be one of the last busy weeks of this earnings season. Investors can expect reports from big-box retailers including Walmart, Target, Home Depot, and Macy’s, which could offer more insight into the third quarter’s robust consumer spending. The Census Bureau will release data on national retail sales for October on Wednesday, indicating whether this momentum continued into the fourth quarter. We’ll get the latest inflation figures with the October Consumer Price Index on Tuesday. Market watchers can expect updates on the housing market, including last month’s housing starts and the NAHB’s Housing Market Index for November. President Biden's meeting in the middle week with China leader Xi Jinping will also be closely watched by investors in the tech sector. Next Friday marks the deadline to avert a government shutdown, 45 days after Congress passed a temporary resolution to keep the government funded through Nov. 17.

On top of that: VIX expiration on Wednesday and Monthly OPEX on Friday. We are definitely in for a big week!

Ransomware attacks are on the rise, posing new challenges to businesses in an age when nearly everything is done online. Another wakeup call this week showed the extent of potential disruptions, with a ransomware attack on one of the world's largest banks interrupting settlements in the U.S. Treasury market. Sources said LockBit, a cyber group with ties to Russia, was behind the ransomware attack on the Industrial & Commercial Bank of China. While the market's overall functioning remained intact, the cyber attack prevented swathes of Treasury transactions from clearing and prompted deals to be rerouted.

Last week in the crypto ecosystem, Poloniex suffered a breach. BlackRock seeks to launch an Ethereum (ETH) ETF as it awaits a decision on the Bitcoin (BTC) application. BTC targeted $38,000 amid a sustained rally.

It was about a week ago when the primary cryptocurrency last dipped below the $35000 line. However, the bulls took over the market at that point and pushed the asset north to almost $36000 almost immediately. After a minor retracement, bitcoin went on the offensive on Thursday and skyrocketed to $38000 for the first time in 18 months. Nevertheless, it failed to maintain this momentum, and the subsequent rejection pushed it back down by over two grand.

The past seven days were quite positive for most of the crypto market. Ethereum was among the leaders in terms of gains due to the speculations that BlackRock will file for a spot ETH ETF in the States. The native token went from $1,900 to a 7-month peak at over $2,100 at one point.

Speaking of speculations, the rumors about FTX finally being able to restart operations under one form or another, which even got a nod from the SEC Chair Gary Gensler, sent the FTT token flying within the same timeframe. Despite a 9% daily retracement, FTT is up by 200% on a weekly scale. The other triple-digit price gainers from the top 100 include ORDI, Celestia, and OX Protocol. Terra, THORChain, Solana, Avalanche, Cronos, and Filecoin follow suit. The total crypto market cap added roughly $100 billion over the past week and stands well above $1.4 trillion.

Macro y news

This Week's Major U.S. Economic Reports:

This Week's Major Eurozone Economic Reports:

Earnings for next week:

U.S Macro data

US Debt Affordability

Moody's released a change to their outlook on US's ratings from "stable" to "negative". A change to the outlook comes 3-6 months before an actual change in ratings if certain conditions are fulfilled. A change does not always follow and the outlook may be changed back to stable or even positive if the situation improves. As a reminder, Moody's is the only big ratings agency that still has the US rating at the highest level which is Aaa.

While this change in outlook may not share up equity and credit markets, the issues raised by Moody's are not altogether benign. The major issues cited are "weakening debt affordability and decline in fiscal strength", brought on by an increase in government spending and "continued political polarization within US Congress".

In terms of Debt Affordability, they are talking about the increasing level of interest expenditure on the ballooning levels of US Debt. It should come as no surprise that the current level of US Debt is the highest it has been in a long time.

But, what's more alarming is that the US is running one of the highest fiscal deficits, which means their expenses or outlays are much higher than their income or receipts.

In fiscal year 2023, which ended on September 30, the federal budget deficit totaled nearly $1.7 trillion, an increase of $320 billion (or 23 percent) from the shortfall recorded in the previous year. Revenues and outlays alike declined from 2022 totals, revenues fell by 9%, or $457 billion, and outlays decreased by 2%, or $137 billion.

This fiscal deficit is expected to increase over the years, primarily driven by interest rate expenses and aging-related entitlement spending. As the level of interest rates in the economy have increased drastically, there's been a huge increase in the interest burden on this debt. The chart below shows us that interest payments will start to overtake the primary deficit in the next 5 years and continue on that path. Primary deficits will continue to remain in the range of 3.3% of GDP while interest costs will triple by 2053.

With more and more of the fiscal deficit being driven by interest payments and mandatory entitlement programs, there will be very little wiggle room in the budgeting process and bipartisan political disagreements will lead to a further reduction in financial flexibility.

Moody's still retains the rating for the US given the country's exceptional economic strength, solid institutional & governance strength and the central role of the US Dollar and Treasury bond bank in the global financial system. However, the rising debt levels and diminishing debt affordability remains a serious concern. Unless there is a meaningful increase in government revenues or a structural reduction in spending, the possibility of a downgrade remains.

Moody's change in US debt outlook to negative comes one week before the November 17th deadline to pass the government spending appropriations bills. If the 12 appropriations are not passed by the House and Senate and signed by the President by November 17th, the US Government will enter into a partial shutdown.

The probability of a compromise solution is likely zero percent, and the best outcome is another extension, a continuing resolution (CR). The moderates from both parties are calling for a "clean CR", but the House ultra conservatives are willing to pass the multistep or "laddered CR", which is unlikely to pass the Senate.

It's difficult to see where the compromise could be reached, the new House Speaker Johnson is unlikely to go for the bipartisan bill like the previous speaker McCarthy. The only area of compromise could be the realization that there is an active war in the Middle East and that the US government shutdown could be a national security issue. But still, a clear CR is unlikely to pass, so what miraculous compromise will be reached remains to be seen.

Investors pay close attention to Treasury auctions

U.S. Treasury debt auctions during the week seemed to play an uncommonly large role in driving sentiment in both the equity and bond markets.Favorably received auctions of three-year Treasury notes on Tuesday and 10-year notes on Wednesday appeared to boost sentiment. However, Thursday's USD 24 billion auction of 30-year U.S. Treasury bonds was met with the weakest demand in two years. Investors have lately been paying close attention to whether demand will be able to keep up with the government’s elevated borrowing needs.

At the auction of government debt that matures in 30 years, investors were awarded 4.769% in yield, 0.051 percentage point higher than the yield in pre-auction trading. The difference between the two yields, called a tail, indicated a weak auction where the U.S. government had to entice investors with a premium over the market to buy their debt. Primary dealers, who buy up supply not taken by investors, had to accept 24.7% of the debt on offer, more than double the 12% average for the past year.

Market participants don’t usually focus on Treasury auctions, given that the government routinely puts billions of dollars of debt up for sale. But investors started zeroing in late this year as questions surfaced about demand for Treasuries. The national budget deficit grew to $1.7 trillion in fiscal 2023, the 12 months through September, making it about $300 billion more than the year before, according to the Congressional Budget Review, an independent research body.

NY Fed Household Debt and Credit report

Household credit stress continued to build in Q3, particularly for credit cards and auto loans, according to the latest NY Fed Household Debt and Credit report.

- Transition into serious delinquency (i.e. 90+ days) continued to rise for all loan types other than student loans & home equity loans. Credit card and auto loan transition rates have surpassed their pre-COVID level and are trending higher.

- The share of loan balances in serious delinquency remained below pre-COVID levels for all loan types but credit cards are rising most rapidly.

- The early transition rate for mortgage delinquencies (i.e. into 30-60 days late) has climbed back to roughly the pre-COVID level along with the transition rate into seriously delinquent.

- Credit card & auto loan stress has been concentrated in younger age groups, with the transition rate into serious delinquency of the 30-39-year-old cohort rising most rapidly and far surpassing the pre-COVID rate.

US growth potentially slowing down

There were very few economic data releases this week, and most were in line with expectations. The one exception may have been the University of Michigan’s release on Friday of its preliminary gauge of consumer sentiment, which fell unexpectedly to its lowest level in six months. According to the survey’s chief researcher, the wars in Gaza and Ukraine added to ongoing concerns about higher interest rates. Long-run inflation expectations also reached 3.2%, the highest level in the survey since 2011.

Median home prices are contracting aggressively.In just 2 years, the % change has gone from over 20% to -7.9%.

This is the sharpest collapse on record,cCurrent levels have occurred ONLY 2 times in the last 60 years:

1. 1970

2. 2008

Both instances ended with equities declining more than 30%.

The US housing market is in a state of deadlock. 30-year mortgage rates recently hit levels unseen in 2 decades. As a result, buying conditions have plummeted to levels seen only once since 1960 which ended in a severe recession.In other words: People don’t want to buy homes now because of the high borrowing costs involved.

Concern over commercial real estate loans, particularly, though certainly not limited to, the office sector, has been driving increasing degrees of uneasiness among bankers, regulators, and the CRE industry. Some new data is further stoking concerns. Delinquency rates for CRE bank loans are hitting levels unseen for the last 10 years.

The last time delinquencies hit this level was in 2013 as the country was stumbling toward recovery in the aftermath of the Global Financial Crisis. There is nothing in the current data suggesting that delinquencies cannot or will not rise higher.

Access to credit is becoming increasingly difficult for businesses. More than 50% of domestic banks are now tightening lending standards. Simultaneously, US interest rates are at the highest level since the pre-Financial Crisis period. Current levels of credit tightening have always ended in a recession.

Bank credit has officially entered contraction territory after witnessing one of sharpest drops on record.Since 1974, this has only happened one time during the 2008 Financial Crisis. Back then, this indicator contracted to levels as low as -5%. At the current rate, a credit event is just a matter of time.

The consumer has borrowed more than they can afford. Default rate on credit card loans from small lenders has seen a sharp spike to 7.51%. This level is the highest level ever seen, even higher than the Dot Com bubble and Financial Crisis. With credit card interest rates still over 20% consumers are going to be overloaded with high costing debt.

Housing defaults are now at the highest levels in a decade.

This has happened only 2 times in the last 75 years, savings as a % of income is now contracting, indicating that people are finding it very hard to save. The last 2 contractions happened in:

- 2008

- 2020

The labor market is weakening, job openings have been collapsing. This type of a decline have occurred 3 times:

1. Dot Com bubble

2. Financial Crisis

3. Covid 19

Each instance ended in a sharp economic downturn. The worst part, this is happening when the consumer is running low on savings.

Job losses have been accelerating aggressively. Current rate of increase is similar to 3 economically volatile periods:

- Dot Com bubble

- Financial Crisis

- Pandemic

Each of these saw a significant rise in the unemployment rate

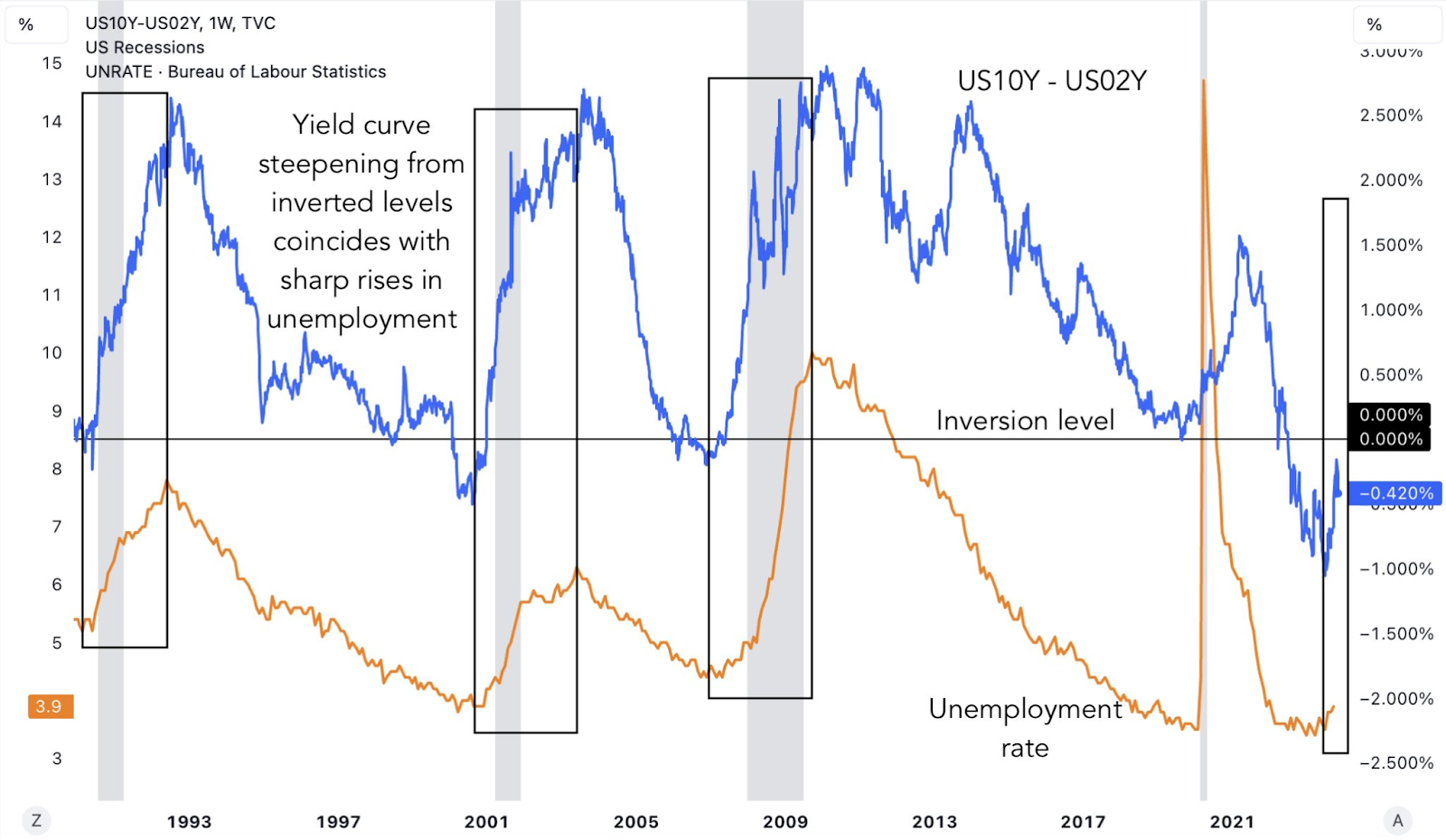

Every time the unemployment rate has crossed above its 24-month moving average, it marked the beginning of a significant deterioration in labor markets.

Yield curve steepening from inverted levels has systematically coincided with sharp rises in the unemployment rate.

Eurozone macro data

European government bond yields broadly climbed as markets wrestled with the prospect of interest rates remaining “higher for longer” after hawkish commentary from policymakers. European Central Bank (ECB) President Christine Lagarde said it will take more than “the next couple of quarters” for the ECB to start cutting rates. The yield on Germany’s 10-year government bond rose above 2.7%. Italian bond yields also ticked higher.

The latest statistics continued to point to a weak European economy. Retail sales in the eurozone fell 0.3% in September, after declining 0.7% in August.

The economic sentiment index produced by the Sentix consultancy came in at -18.6 in November, an improvement from the -21.9 recorded in the previous month.

In Germany, industrial production in September fell 1.4% sequentially, after flatlining in August, while manufacturing orders increased 0.2%, well below the 1.9% registered in the previous month. In France and Italy, industrial output was flat in September compared with August.

UK macro data

Bank of England (BoE) Governor Andrew Bailey said at a central bank conference in Ireland that it was “really too early” to talk about cutting interest rates. He spoke after BoE Chief Economist Huw Pill said that financial markets pricing in an initial rate cut in August next year “doesn’t seem totally unreasonable,” which triggered a sharp decline in short-dated government bond yields.

UK gross domestic product (GDP) in the third quarter matched the BoE’s forecast for zero growth, after expanding by 0.2% in the prior three months. Monthly GDP was better than expected, with the economy expanding 0.2% in September. GDP growth in August was revised down to 0.1% from 0.2%. The Office for National Statistics said growth was driven by expansion in engineering, healthcare sales, and machinery leasing, which offset falls in health, management consultancy, and commercial property rental.

Japan macro data

The yen weakened past the 151 level to the U.S. dollar, from around 149 the prior week, depreciating to its lowest in around 33 years. Investor risk appetite was dampened toward the end of the week by hawkish comments from Federal Reserve Chair Jerome Powell, who said that the U.S. central bank won’t hesitate to tighten monetary policy further if needed to contain inflation, raising expectations that interest rates will remain higher for longer.

Bank of Japan (BoJ) Governor Kazuo Ueda warned that normalizing short-term interest rates will be a serious challenge, due to the potential impact on financial institutions, borrowers, and aggregate demand. Speaking at a conference organized by the Financial Times news organization, he said that it is too early to determine what specifically the central bank will do when it normalizes its policy stance. He added that the bank is making progress toward reaching its 2% inflation target.

The yield on the 10-year Japanese government bond (JGB) fell to 0.85%, from 0.91% at the end of the previous week. JGB yields remained elevated, however, following the BoJ’s October adjustment of its policy of yield curve control, the second tweak in three months. Effectively allowing yields to rise more freely, the central bank now regards its 1.0% ceiling for 10-year JGB yields as a reference, rather than strictly capping interest rates at that upper bound. However, Governor Ueda has repeatedly stated that the 10-year JGB yield is unlikely to rise significantly above 1.0%.

Japan’s cabinet approved an extra budget to support Prime Minister Fumio Kishida’s latest economic stimulus package, which is worth more than USD 110 billion. Measures include cuts to income and residential taxes as well as cash handouts to low earners to ease the impact of inflation on households and reinforce wage increases. Japan’s inflation-adjusted real wages dropped in September while consumer spending also declined, reflecting the squeeze on individuals’ purchasing power that is stoking voter dissatisfaction.

China macro data

The consumer price index fell 0.2% in October from the prior-year period, after remaining unchanged in September, as lower pork prices weighed on food prices. Meanwhile, the producer price index dropped 2.6% from a year ago, marking the 13th consecutive month of decline.

Trade data offered a mixed snapshot of China’s economy. Overseas exports declined 6.4% in October from a year earlier, surpassing the 6.2% fall in September, amid weaker global demand. However, imports unexpectedly rose by 3%, reversing the 6.2% contraction in September and marking the first year-on-year growth since September 2022. Overall trade surplus fell to a below-consensus USD 56.5 billion, down from September’s USD 77.71 billion.

The latest readings underscored the fragility of China’s economy and appeared to add to concerns that growth has not yet bottomed. Despite Beijing’s recent efforts to prop up demand, many economists predict that the government will introduce further stimulus measures to counter deflationary pressures.

Crypto News

=> BlackRock, the world's largest asset manager, seeks to list an ETF that holds Ethereum's ether (ETH), deepening its commitment to cryptocurrencies. The plan was revealed in a filing by Nasdaq, where BlackRock will seek to list the product. This disclosure massively drove the price of Ethereum past $2,000.

However, the company has already made waves in crypto by seeking to list a Bitcoin ETF, which the community sees as a “done deal.” According to the new filing, Coinbase would be the custodian for the ether held by the product. BlackRock also has a market-surveillance pact with Coinbase. The filing appeared to try and preempt possible SEC objections to the surveillance-sharing aspect.

=> The U.S. Securities and Exchange Commission (SEC) has opened talks with Grayscale Investments on the details of the company's application to convert its trust product GBTC to a spot bitcoin exchange traded product (ETF), according to a person familiar with the back-and-forth, which could have momentous implications for the crypto industry.

An SEC approval of one or more ETF applications is keenly awaited by the sector, which sees that moment as a milestone that could ease everyday investors' path into digital assets. Grayscale has been in contact with both the SEC's Division of Trading and Markets and the Division of Corporation Finance since winning its court fight, said the person, who requested anonymity because the talks remain private. Both SEC divisions would have a role in shaping and approving the firm's ETF application. Grayscale and CoinDesk are part of the same parent company, Digital Currency Group.

Grayscale has long had a relationship with the SEC due to its existing Grayscale Bitcoin Trust (GBTC), but when it sought to launch an ETF that would carry direct crypto assets, the agency denied it. A U.S. federal court battle ensued that ended with a panel of judges finding the SEC was "arbitrary and capricious" in its rejection, and the court ordered the agency to erase its denial. The court decision was finalized last month, putting the application back in front of the regulator.

=> The SEC took the spotlight again, making headlines for its decision to oppose Binance’s motion to dismiss the regulator’s lawsuit. Recall that Binance previously filed a motion to dismiss the charges.

Former SEC official John Reed Stark disclosed the SEC’s opposing response, which cited remarks from a former Binance Chief Compliance Officer, in which he claimed that the company was operating an unregistered securities exchange in the U.S. As it opposed the motion, the SEC deemed the company’s arguments as nothing short of “absurd.” In a rather direct response, the Commission reaffirmed its stance that the majority of crypto assets fall within the realm of securities.

=> The Celsius bankruptcy plan has been approved, allowing customers to receive shares in the reorganized company, NewCo, and around $2 billion in Bitcoin and Ether to be redistributed to Celsius creditors. Many of the creditors were participants in its Earn program, which allowed them to earn weekly rewards by holding CEL tokens that were locked for a year.

NewCo will expand the existing mining operations of former crypto lender Celsius and will be managed by the Fahrenheit consortium. However, the former CEO, Alex Mashinsky, was arrested in July 2023 on charges of securities fraud, commodities fraud, and wire fraud.

=> U.S. Banking Watchdog Hsu says tokenization is promising, but crypto is full of fraud. Michael Hsu, the acting chief of the U.S Office of the Comptroller of the Currency that oversees banks, is excited about the possibilities of tokenization to solve settlement problems.

=> Hong Kong is assessing whether to allow exchange-traded funds that invest directly in crypto as officials step up efforts to create an Asia-Pacific digital-asset hub while tackling the fallout of the JPEX scandal. The city is weighing retail-investor access to such spot ETFs providing regulatory concerns are met, Securities and Futures Commission Chief Executive Officer Julia Leung said.

=> The approval of Ripple’s XRP by the Dubai Financial Services Authority (DFSA) could pave the way for XRP's integration into digital asset services within the Dubai International Financial Centre (DIFC), a major financial hub in the Middle East.

=> UK moves closer to Stablecoin Regulation with new FCA and BOE documents

=> EU watchdog sets out capital, liquidity rules for stablecoin issuers. The European Union's banking watchdog set out proposals on Wednesday 8th requiring that from June issuers of stablecoins backed by currencies to have sufficient funds to fully redeem investors.

The bloc is deploying the world's first comprehensive set of rules for cryptocurrency and stablecoin markets, and the European Banking Authority (EBA) proposed minimum capital and liquidity requirements for issuers of stablecoins and other types of digitized tokens.

The EBA launched public consultations on liquidity requirements for the reserve of assets that back a stablecoin, meaning that only eligible assets of high enough quality can be used.The aim is to ensure that the assets can be quickly sold to raise cash for paying redemptions even in stressed markets, key to stopping runs and contagion in a crisis. The EBA said that issuers of stablecoins backed by a currency must be able to offer full redemptions at par to investors.

=> Binance, the world’s leading cryptocurrency exchange, has announced that users can now trade Ordinals (ORDI), a BRC-20 token collection minted on the Bitcoin blockchain, against Tether USDT, Bitcoin BTC, and the Turkish lira. As noted, the ORDI token has no listing fees, and withdrawals will open on Nov. 8. To incentivize users, the first 1,000 who deposit at least 72 ORDI to the exchange will receive a 50 USDT trading rebate voucher.

Within the same week, Binance also launched its new Web3 wallet, using multiparty computation (MPC) to break a user's private keys into three smaller parts, two of which will be controlled by the user for self-custody.

=> Poloniex, a digital asset exchange, has been hacked, with over $100 million in crypto being drained by attackers. Blockchain security firms believe that the incident was due to a “private key compromise.” Moreover, the exchange stated that it maintains a healthy financial position and will fully reimburse the affected funds. Justin Sun, the billionaire entrepreneur who acquired the exchange in 2019, also posted the same assurance. Sun also offered a 5% white-hat bounty to the Poloniex hacker and claimed that he is looking for collaborations to recover the lost funds.

=> DZ Bank, ranked as Germany’s third-largest bank by assets, has announced the introduction of its blockchain-based digital asset custody service. In a press release dated November 2, the bank detailed its plans to cater to institutional clients by offering them digital securities, like the cryptocurrency bond from Siemens that DZ Bank had previously invested in six months prior.

=> Crypto Funds experience a six-week streak of Inflows.

=> Stablecoin USDC issuer Circle is reportedly in talks with its advisors about an Initial Public Offering (IPO) for early next year.

The next several weeks will be very interesting for Bitcoin, here’s the latest ETF 19b-4 deadlines:

Cryptos: spot, derivatives and “on chain” metrics

A lot can change in the cryptocurrency market within the span of the week, which has been the case now. On Tuesday, the primary digital asset fell to $34500 after failing to overcome the $35000 level despite a few attempts. However, the bulls took charge at this point and drove Bitcoin north hard. Two days later, the asset shot up to $38000 for the first time in a year and a half. It was violently rejected there and dumped by over two grand within hours. Nevertheless, it bounced off and spiked to $37,500 yesterday. It has been unable to maintain its run since then, but it still trades above $37,000 as of now.

This means that its market capitalization is still above $725 billion, but its dominance over the alts has taken one more hit and is down to 51%.

Ethereum was among the top performers in the past few days as BlackRock registered a trademark in Delaware to potentially file for a spot ETH ETF in the States. The second-largest digital asset shot up by over $200 in hours and marked a 7-month high at over $2,100.

On the other hand, XRP, LINK, ADA, and LINK are with minor gains. Solana, Dogecoin, Tron, Polkadot, Shiba Inu, and Avalanche, though, have skyrocketed by more impressive percentages. In the case of SOL and SHIB, the gains are by double digits.

FTT, however, is the week top performer. FTX’s native token has soared by 45% daily and 250% weekly. This comes amid rumors indicating that the exchange could be revived soon. Even the SEC’s chair laid out the conditions under which FTX could be reactivated.

The total crypto market cap has reclaimed the $1.4 trillion spot amid the latest price rallies.

Gainers / Losers last 7 days, block size volume.

Bitcoin

The market after a first bullish imbalance failure of the lower major structure managed to defend itself, broke through the $28100 VPOC and started a powerful breakout of the upper range. Demand has fully taken control, there is no doubt, however the verticality of the move and some overheated metrics in derivatives makes us be extremely cautious and think that we may be in a short term market climax.

Last week we were looking for retracements to validate the bullish imbalance of the intermediate structure, however the market has refused to correct in the slightest to look for such a setup. We continue to insist that we want to see an effective bullish imbalance of the intermediate structure. Such an imbalance has to be above the previous highs preventing the price from re-entering the range.

The market is in climax and certainly in fomo buying rumors not news, be aware of this situation and be careful.

Bitcoin 06/11/23 4h chart

Bitcoin 13/11/23 4h chart

In a low time frame chart we observe a sloping value area with a shakeout event and its consequent secondary test, which is leaving a possible distributive structure. For this week, important for the rest of the risk markets, we expect a visit at least to the VPOC of $34500. At that point, some demand reaction is to be expected. On the contrary, if sellers manage to break this VPOC, the whole structure shown in this chart will rotate to distributive.

Bitcoin 13/11/23 5 min chart

In high timeframe charts, we are aware that we are at a key and pivotal moment for Bitcoin on a longer time horizon.

- Despite the first bullish imbalance failure of the structure marked in green, it has managed to defend itself and eliminate the weakness of demand.

- It has broken the VAL (value area low) of the distributive structure marked in red.

- It has broken the VWAP anchored at all time highs (ATH).

- It has tested the distribution´s VPOC ($38000) after breaking the VAL.

- All of this would clearly mark a complete change in behavior after the sharp declines of 2022.

Bitcoin 06/11/23 Daily chart

Bitcoin 13/11/23 Daily chart

Ethereum

Ethereum price surged above $2,000 on Thursday, November 9th, after BlackRock confirmed plans to launch an Ethereum Spot ETF in a NASDAQ filing. On-chain data shows that a price-savvy group of large institutional investors spent the weekend buying up millions of dollars worth of ETH, likely in response to the bullish news event.

Ethereum, after having remained for several weeks in the demand zone marked on the chart without any response, has finally managed to wake up from its lethargy. Right now we are in the sellers' initiative zone, which has previously left several rejections. The bulls must conquer this zone, reversing the rejection price action. A clear breakout and consolidation above this zone would open the door to a very promising long term bullish scenario.

Ethereum 06/11/23 4h chart

Ethereum 13/11/23 4h chart

Classic markets

We repeat what we commented last week:

Actual market behavior: "positive" catalyst ("dovish" Powell) => crunch vol + buy tech + squeeze options bearish positioning + YOLO (Xmas rally, presidential cycle, AI bull market, CTA max short and now max long, this time is different) => Sell Off => repeat until something serious happens and really breaks something.

It should be clear to the reader that there is no “alpha” in buying Nvidia or The tech sector / Magma 7. It is the same trade as short VOL.

The recent market squeeze was driven by a massive unwinding of hedges (gamma squeeze) and short positions, and that it does not reflect a fundamental improvement in the economic and geopolitical outlook, which remains highly uncertain and volatile. The financial and economic systems are still in a peak speculative bubble that is vulnerable to shocks from inflation, bond yields, deficits, political dysfunction, Chinese bubbles, the US-China rivalry, and conflicts in Ukraine and the Middle East.

Stocks had a big rally day on Friday, but most of the week was a real struggle. The rally on Friday didn’t help the equal-weight SP500 (RSP) or Russell 2000 finish positive for the week, despite the SP 500 and the Nasdaq 100 finishing higher by more than 1 and 2%, respectively. It appears to be more of the same, with just a handful of stocks continuing to power the major indexes higher while the rest of the market is left behind.

SPX is now outperforming RSP by over 1400 basis points YTD.

Year to date 2023 returns:

Nasdaq 100 (QQQ) +40.1%

SP 500 (SPY) +15.1%

Dow Industrials (DIA) +4.4%

Equal-Weight S&P (RSP) +0.4%

Russell 2000 (IWM) -1.7%

It’s remarkable how today’s lack of leadership in the stock market echoes the period preceding the tech bust. As shown in the chart below, technology companies were the only sector holding up the market from mid-1999 to March 2000. Those times were strikingly similar to today.

Tech's share of equity sector mutual fund assets has never been higher.

2023 has been the polar opposite of 2022:

- Worst performing areas of the equity market in 2022 (Nasdaq/Tech/Growth) have been the best performers in 2023.

- Best performers from 2022 (Energy/Value/Equal Weight) have been the worst in 2023.

This is the widest alligator jaws ever observed: Nasdaq breadth at all time lows, while a few Nasdaq companies keep pushing the Index higher.

If you exclude the Mag 7, the market actually makes sense.

However, this week will feature a lot of important economic data, including the CPI, retail sales, and the PPI. Additionally, Wed morning will be the VIX OPEX, and Friday will be the monthly OPEX, and all of this combined could leave the markets with big swings.

On top of that, on Friday, Moody’s Put the US credit rating on negative watch, which puts the US one step closer to a credit rating downgrade, which is a pretty big deal and could mean that bond yields start moving higher again. Additionally, Tuesday’s CPI report seems fairly important, given that we are going to see the health insurance component of CPI reset.

MAG-7 PE looks way too high vs Real Yields. We expect a hot US CPI on Tuesday 14th, this will put heavy pressure on the Risk Premium GAP to close.

VVIX / VIX is back within trend and falling. Right on schedule for OpEx week. We should see a reaction in volatility after VIXpiration on November 15th.

Options, Gamma and IV

This week's economic data comes as dealers are stuffed with gamma at the 4,400/4,450 strikes. This could hinder if not reverse the upside progress seen. In case you might be new, when participants sell (monetize) calls, MM are selling the deltas (stock/futures) back to the market.

This VIX OPEX is heavily skewed to ITM puts. As CPI is Tuesday 11/14 and the VIX is down 33% since the recent peak, further monetization of ITM puts will take place. This temporarily removes the suppression and upward pressure in the VIX complex can be felt.

When you combine SPX and VIX OPEX monetization, if U.S. CPI surprises to the upside, the mechanics of selling ITM positions and the opening of new bearish positions could bring great risk to the bulls progress.

At the same time, let's not forget that these diabolical mechanics that the market has found to perpetuate its favorite trade (long tech, short vol) have led participants to perceive no risk at all, leaving tail risk, as shown in the SKEW, completely forgotten.

Market Comment

Bear market rallies are notoriously violent and abrupt. And this last one was among the most violent and abrupt of them all. There is no greater risk situation in which the risk is not perceived. The prevailing market dynamics have managed to make the rest of the participants believe that there is no risk in sight, all this at the gates of a recession and in the most turbulent geopolitical environment since World War II.

Although the reader may think that last two week's rally is due to a real show of buying strength, unfortunately this is not the case. An epic gamma short squeeze drove stocks higher two weeks ago, driven by a compilation of factors that aren't likely to persist.

Little has changed from last week. After the massive short gamma squeeze, the market has rested, the shift to a positive gamma regime has used up all the gas and now the market maker is pushing for a break above the Gamma Call wall at 4400-4450.

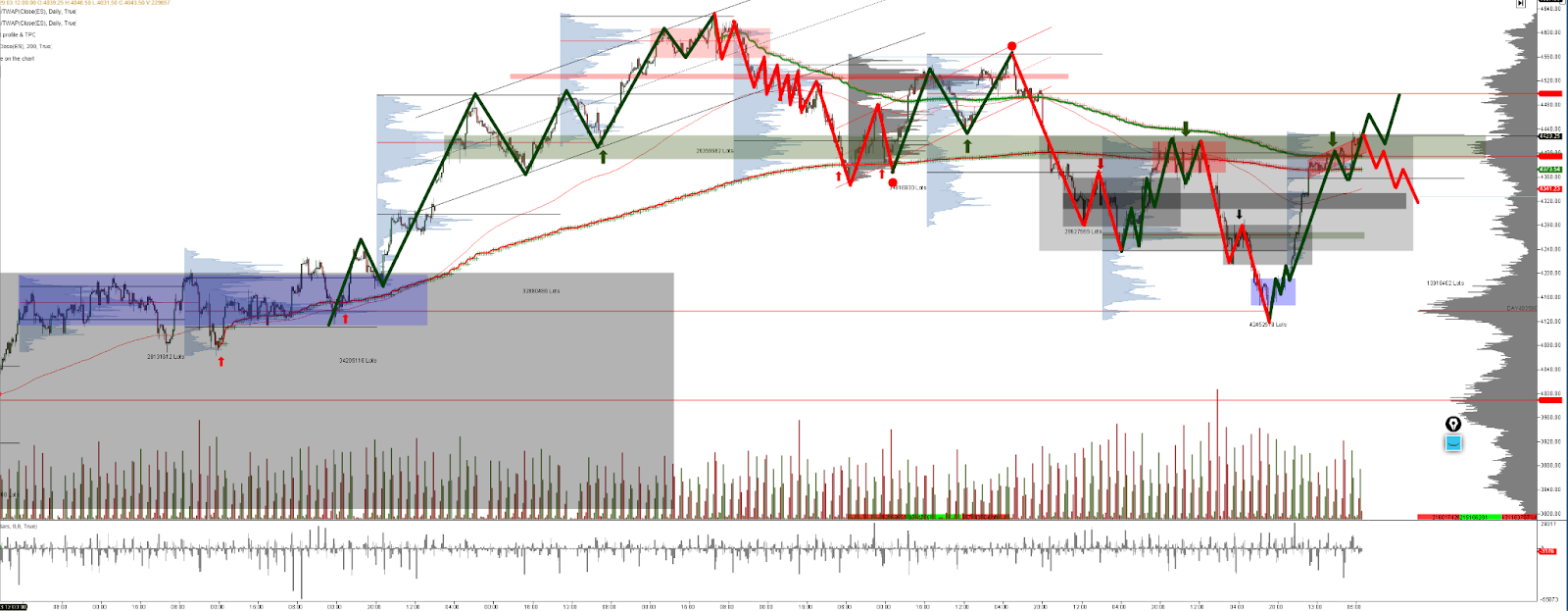

In this high time frame chart, the battles to be won by buyers and sellers are very clear. Bulls must consolidate above the green VWAP anchored at highs and recapture the upper HVN coincident with the June VPOC (area marked in green). On the other hand, sellers, although far from taking control, the market's nefarious structure and auction in this rally could make things easier for them. Let's go down in time frame to analyze it in detail.

ES_F 4h chart 06/11/23

ES_F 4h chart 13/11/23

Last week's market lateralization is leaving a minor steep slope structure marked in red. We believe this structure will resolve as distributive with this week's events (U.S. CPI, Vixpiration and monthly Opex). For sellers it is key that the market loses the previous buying control (marked with the black arrows), if so, the rally will fade at the same speed as it was created. It's not how far the market goes, but the way it goes, poor market auction and short gamma squeezes are always repaid.

ES_F 1h chart 13/11/23