.png)

.png)

Summary

As expected, the U.S. Federal Reserve returned to rate hiking mode after pausing in June, as it lifted its key benchmark rate by a quarter-percentage point to the highest level since 2001. The increase to a range between 5.25% and 5.50% was the 11th hike since March 2022, when spiking inflation led the Fed to lift rates from a near-zero level. Markets had already anticipated the move and as such, there was little volatility in both equities and the crypto market.

The FOMC statement went on to note that “recent indicators suggest that economic activity has been expanding at a moderate pace.” Nonetheless, the Fed intends to continue assessing lagging economic indicators and new information before finally deciding whether or not it will implement any more rate hikes this year.

On the brighter side, even as the macro picture remains slightly uncertain, the Fed staff is no longer forecasting a recession which means inflation could eventually come down without more significant downturns to the global economy. We have serious doubts about this statement and see the “soft landing” scenario, which is beginning to be widely accepted, as really complicated.

The Bank of Japan has made a tweak to its yield curve control policy, it decided to keep the official cap of the 10 years bond at 0.5%, while allowing more flexibility with the new, so-called strict cap, and raise the trading band to +/- 1.0%.

The European Central Bank (ECB) raised its key interest rate to 3.75% while also signaling that it could soon pause its rate hiking cycle as soon as September. While 3.75% is the ECB’s highest level in 22 years, that rate remains well below the U.S. Federal Reserve’s current benchmark rate range of 5.25% to 5.50%.

Near the midpoint of earnings season, companies in the S&P 500 were on track to record an overall decline in their profit margins for the sixth quarter in a row. The average net profit margin halfway through earnings season was 11.1%, versus 12.2% in the same quarter a year earlier, according to FactSet. Margins peaked at 13.0% in the second quarter of 2021.

Earnings season continues next week with reports due from some of the market’s most widely held names, including Apple and Amazon, among others. We’ll get the latest updates on the labor market, including the Job Openings and Labor Turnover Survey (JOLTS) for June, ADP’s National Employment Report, and the July nonfarm payrolls report. PMI readings from S&P Global and the Institute for Supply Management (ISM) will also become available, along with inflation and GDP readings from the eurozone, and an interest rate decision from the Bank of England (BoE).

Top coins like Bitcoin and Ethereum had a quiet price performance this week. However, there are some exciting developments and challenges that filled up the cryptocurrency world in the past seven days. Regulatory initiatives remained in focus, with the passage of a pro-crypto bill in the US Congress garnering attention.

During this weekend, it has been reported that Curve, a prominent decentralized finance (DeFi) platform built on the Ethereum blockchain, has fallen victim to a significant exploit. The platform's vulnerability to a "re-entrancy" bug in the Vyper programming language has exposed upwards of $100 million worth of cryptocurrency to potential risk. The exploit resulted in the draining of several stablecoin pools on the Curve system, which play a crucial role in pricing and liquidity for various DeFi services.

The exploit has had a destabilizing effect on the trading markets for Curve's native CRV token. As a result of the attack, the CRV token's value plummeted by 17% within a single day. The market seems to have digested this exploit, however, the exact scope of this vulnerability and its implications on the broader DeFi ecosystem is yet to be fully assessed.

Macro y news

Earnings for this coming week:

U.S Macro data

As expected, the Fed raised interest rates by 0.25% at its July FOMC meeting, bringing the fed funds rate to 5.25% to 5.5%. Notably, Fed Chair Jerome Powell was careful not to declare “mission accomplished.” He emphasized that no decision had been made on future rate hikes or on the September meeting.

The Fed and markets will digest two additional CPI inflation readings and two U.S. jobs reports between now and the Sept. 20 meeting. This will help determine the path of interest rates going forward.

While the Fed may be toward the end of its rate hikes, we believe rate cuts remain unlikely this year. The Fed may signal rate cuts early next year if inflation continues to move toward a 2% target, as the fed funds rate at current levels remains in restrictive territory versus a potential neutral rate of around 2.5%. Thus, we expect to continue to see the Fed on an extended rate pause through the beginning of 2024.

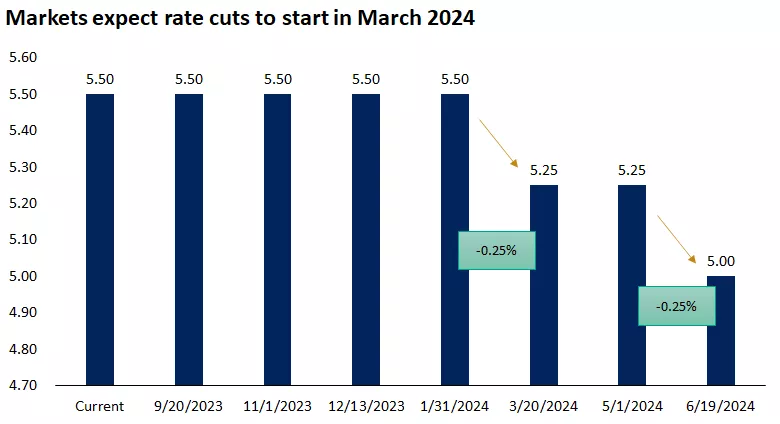

According to the CME FedWatch Tool, futures markets ended the week pricing in only a 27.4% chance of further rate hikes by the end of the year compared with a 90.8% chance the week before.

FOMC highlights:

Fed: tighter credit conditions are likely to weigh on economic activity, hiring and inflation, extent to which remains uncertain.

Fed: vote in favor of policy was unanimous

Fed: we will continue to reduce our bond holdings as described in previously announced plans.

Fed to consider extent of additional firming to curb inflation.

Fed says recent indicators suggest economic activity has been expanding at a 'moderate' pace vs 'modest' pace in june statement

Fed's Powell: the Fomc is to take a data-dependent approach on future hikes.

Fed's Powell: the full effects of tightening are yet to be felt.

Fed's Powell: the housing sector picked up but well below 2022 levels.

Fed's Powell: growth in consumer spending has slowed from earlier in the year.

Fed's Powelll: labor market remains very tight.

Fed's Powell: inflation has moderated somewhat.

Fed's Powell: process of getting inflation to 2% has a long way to go.

Fed's Powell: the Fomc will take cumulative tightening and lags into account.

Fed's Powell: i have been seeing effects of tightening in some sectors.

Fed's Powell: we haven't made a decision to go every other meeting.

Fed's Powell: we haven't made any decisions about any future meetings.

Fed's Powell: if data suggests more hikes are needed that is the judgment we will make.

Fed's Powell: it's possible we'd raise in September if data warrants it.

Fed's Powell: we believe monetary policy is restrictive.

Fed's Powell: at margin, stronger growth could lead to more inflation.

Fed's Powell: the totality of the data is important with a particular focus on progress on inflation.

Fed's Powell: we will be looking to see if signal from the June cpi is replicated.

Fed's Powell: we're going to be careful about taking too much signal from one single reading on inflation.

Fed's Powell: how do you balance the risks of doing too much and too little, and we're coming to a place where there are risks on both sides.

Fed's Powell: core inflation is still pretty elevated.

Fed's Powell: some softening in labor conditions is still the likely outcome.

Fed's Powell: policy not restrictive enough for long enough.

Fed's Powell: inflation has proven more resilient than expected.

Fed's Powell: this is not an environment where the Fomc should provide lots of forward guidance.

Fed's Powell: we need to take both the level of inflation and speed of decline in judging when to cut rates.

Fed's Powell: the staff are no longer forecasting a recession.

Fed's Powell: several on the Fomc say they expect rate cuts next year.

Fed's Powell: the Fed won't be cutting rates this year.

Fed's Powell: i'm not using the term optimism, but there is a path to soft landing.

Fed's Powell: I don't see inflation back at 2% until about 2025.

The Fed’s preferred inflation gauge, the core (less food and energy) personal consumption expenditures (PCE) price index had risen 0.2% in June, down from 0.3% in May, making for a year-over-year increase of 4.1%, a tick lower than expectations and the slowest increase since September 2021.

The employment cost index, closely watched because of policymakers’ continued concern about wage inflation, rose 1.0% in the second quarter, also below consensus and the smallest increase in two years.

The Commerce Department reported that the economy had expanded at a year-over-year pace of 2.4% in the quarter, well above both the previous quarter’s growth rate of 2.0% and consensus expectations of around 1.8%. Both businesses and consumers appeared to remain in good shape and spending freely. Durable goods orders jumped 4.7% in June, while personal spending rose 0.5%. Pending home sales also rose unexpectedly.

Eurozone macro data

The ECB raised rates by 0.25%, its ninth consecutive rate increase, bringing their policy rate to 3.75%. As with the Fed, the ECB left the door open for a pause in rate hikes at the September meeting. Inflation in the region, while elevated, has eased to 5.5%, down from around 11% in October 2022.

ECB deleveraging continues. Ahead of this week's meeting, ECB shrink its balance sheet by €18.6bn to €7,186.9bn as matured bonds were not replaced by new ones. ECB's total assets are now equal to 53% of Eurozone GDP vs Fed's 31%, SNB's 121%, BoJ's 129%.

Eurozone bond yields climbed on concerns that the prospect of higher Japanese yields (see Japan section for details) could prompt an exodus of Japanese investors from that market, but yields steadied as the week wound down. The yield on Germany's 10-year sovereign bond, for example, rose above 2.56% before finishing the week around 2.49%. Swiss and French bonds experienced similar volatility.

Annual inflation in the euro area came in at 5.5% in June, down from 6.1% in May but still well above the ECB’s 2% target. Preliminary July inflation readings at a country level provided mixed messages. Data showed that price growth in France cooled more than expected to 5% in July from 5.3% in June. However, adjusted Spanish inflation came in at 2.1% in July, up from 1.6% in June and against expectations of another flat 1.6% print.

Data released in the week showed a slowdown in regional business activity. The Flash Eurozone Composite PMI Index, an initial gauge of activity in the manufacturing and services sectors, fell to an eight-month low of 48.9 in July from 49.9 in June. At a country level, Purchasing Managers’ Index (PMI) readings in France and Germany were both weaker for the month.

German economic growth stagnated in 2Q 2023 after two consecutive quarters (1Q 2023 and 4Q 2022) of contraction. It's the longest quarterly streak of recession/stagnation for Germany since the 2008-09 global financial crisis.

German GDP(qoq) (q2) actual : -0.2% vs -0.3%previous; est 0.1%

German GDP (yoy) (q2) actual : -0.6% vs -0.2%previous

Eurozone preliminary July HCOB Eurozone Manufacturing PMI 42.7 vs 43.5 expected and 43.4 prior

Eurozone preliminary July HCOB Eurozone Services PMI 51.1 vs 51.5 expected and 52.0 prior

Germany preliminary July HCOB Germany Manufacturing PMI 38.8 vs 41.0 expected and 40.6 prior

Germany preliminary July HCOB Germany Services PMI 52.0 vs 53.1 expected and 54.1 prior

France preliminary July HCOB Manufacturing PMI 44.5 vs 46.0 expected and 46.0 prior

France preliminary July HCOB Services PMI 47.4 vs 48.4 expected and 48.0 prior

In Germany, the IFO business climate index fell for the third straight month to 87.3 in July from 88.6 the previous month.

ECB Q2 Lending Survey: The net decrease was again substantially stronger than expected by banks in the previous quarter. Rising interest rates and lower financing needs for fixed investment were the main drivers of reduced loan demand.

Japan macro data

Following its July 28–29 monetary policy meeting, the BoJ decided to keep its key short-term interest rate unchanged at -0.1% and that of 10-year JGB yields around zero percent. It judged that a sustainable and stable achievement of its 2% price stability target had not yet come in sight.

However, the central bank surprised investors with the announcement that it would conduct YCC with greater flexibility to enhance the sustainability of monetary easing under the current framework. While it will continue to allow 10-year JGB yields to fluctuate in a range of around plus and minus 0.5% from the zero percent target level, greater flexibility means that it will regard the upper and lower bounds of the range as references, not as rigid limits, in its market operations. The BoJ will also offer to buy 10-year JGBs at 1.0% (changed from 0.5%) every business day through fixed rate purchase operations.

Tokyo core-core CPI inflation printed at +0.575% MoM. That's the 2nd biggest monthly increase since Covid. And one of the biggest monthly increases over the last 30 years outside of sales tax hikes. Inflation is not transitory in Japan

China macro data

Beijing signaled it will provide more stimulus to support the economy. The Communist Party’s Politburo, China’s top decision-making body led by President Xi Jinping, pledged to provide stimulus to boost domestic consumption amid a flagging recovery after the end of pandemic lockdowns in December. Officials also vowed to enhance support for the ailing real estate sector following the Politburo’s latest meeting, during which leaders set economic policy for the rest of 2023. Despite signaling a pro-growth stance, however, the post-meeting statement contained no specific policy measures.

China’s gross domestic product is projected to expand 5.2% this year, down from previous estimates of 5.5%, while growth for 2024 is forecast to expand 4.8%, according to economists surveyed by Bloomberg. The revisions came after China recently reported its economy grew at a slower-than-expected pace in the second quarter amid weakening domestic and external demand.

Profits at industrial firms declined 8.3% in June from a year earlier, a slower pace than the 12.6% drop recorded in May, according to China’s statistics bureau. Industrial profits fell 16.8% from January to June from a year earlier, better than the 18.8% drop recorded in the first five months of 2023. Despite an overall improvement in manufacturing activity, profits have been under pressure as recent data indicated that China is on the verge of slipping into deflation.

China’s Debt Ratio hits record, masking slowdown in borrowing.

Bonus macro data: US fiscal cliff

The Fed just raised interest rates to their highest level since 2001. Last time interest rates were this high, the US had $6 trillion of debt. Today, the US holds roughly $31.5 trillion of debt. As rates hit new highs, interest on US debt has become a crisis. US interest expense is about to hit $1 trillion for the first time in history. Soon, interest expense will account for over 20% of the entire US government's revenue.This is clearly an unsustainable path.

In June 2023 alone, the US spent $70 billion on interest expenses. This is more than education and veterans' benefits combined. Soon interest expenses will be higher than national defense spending.

For over 20 years, the US has had debt with a historically low interest rate environment.This meant that interest expense on US debt was relatively controlled, even with skyrocketing debt levels. Now, as rates rise at the fastest pace in history, the problem is accelerating.

Over the next 10 years, interest costs are projected to hit $10.6 trillion.Over the next 30 years, the CBO projects interest to total $71 trillion.Interest expense is expected to surpass defense spending in 2029, Medicare in 2046, and Social Security in 2051.

By 2053, interest costs are expected to take up 35% of all government revenues. Within the next 10 years, projections show total US debt hitting $50 trillion. This would mean a $45 trillion increase since the year 2000.

In 30 years, interest costs are expected to be 3 TIMES the cost of R&D, infrastructure and education combined.If inflation persists longer than expected or another inflationary event arises over the next 30 years, these projections will rise rapidly.

Bonus macro data: credit crunch?

Bank credit and leading economic indicators are shrinking at the same or greater rate than in previous recessions. In the major economies of the US and Europe, quarterly surveys are showing that credit is becoming harder to obtain. In the past, a tightening of credit has been a clear indicator of an impending economic downturn. This is quite intuitive because if the prices of houses and cars don’t keep pace with wages and credit dries up, there’s no way for prices to go down. There aren’t many signs of a credit card deficit yet, but we wonder how much consumers can reduce before this crisis begins. Credit card debt in the US has just reached a trillion dollars.

The stock of bank lending to commercial and industrial companies fell in June for the fifth straight month, falling nominal bank lending is not normal in a growing economy.

Bank credit contracting only the second time ever this severe.

The top 10% ex-financial companies by market cap haven't seen interest costs rise, while the bottom 40% have seen a significant rise.

U.S. Consumers are in bad shape. Credit card balances in America are at 20-year highs as interest rates skyrocket.

40% of US adults now have less than $1,000 in savings. Per the NY FED, rejections on consumers applications are increasing.

Crypto News

Top coins like Bitcoin and Ethereum had a quiet price performance this week. However, there are some exciting developments and challenges that filled up the cryptocurrency world in the past seven days.

=> Binance and CEO Changpeng Zhao (CZ) plan to challenge CFTC charges filed in March 2023 for US commodities and compliance law violations. The CFTC alleges the crypto company operated an unregistered derivatives exchange in the US, and CZ and Samuel Lim, the former compliance officer, used a deceptive compliance program.

In their 49-page motion, Binance argues that the CFTC's charges go beyond its authority, targeting foreign entities and activities. They demand the court to drop counts 1 - 6 as "impermissibly extraterritorial." Moreover, they call for Count VII's dismissal, claiming the CFTC is testing a novel claim against an industry that didn't exist when the regulation was formed.

=> United States prosecutors have dropped criminal campaign finance charges against Sam Bankman-Fried (SBF), former CEO of defunct crypto exchange FTX. The decision was said to have been influenced by complexities arising from the US-Bahamas extradition treaty. Meanwhile, SBF argued his campaign contributions weren't part of the extradition document.

=> Crypto exchange FTX and lender Genesis reach an in-principle agreement to settle their bankruptcy case. The agreement aims to resolve claims made by both firms against each other, pending motions, and objections. Though specifics remain undisclosed, it's a significant step forward for the bankrupt entities.

FTX had initially claimed $4 billion owed by Genesis, later revising it to $2 billion. Genesis, filing for Chapter 11 protection after a crypto hedge fund collapse, is FTX's largest unsecured creditor with $226 million owed. However, the settlement will hopefully bring closure to the legal dispute and foster a more stable crypto industry future.

=> The United States House Committee has approved clear regulations for digital assets, a significant step towards establishing a comprehensive regulatory framework in the country. Interestingly, crypto advocates celebrate the long-awaited regulatory progress and despite some Democratic differences, the bill advanced with bipartisan support.

=> The House Financial Services Committee convened again on Thursday, passing a regulatory framework for stablecoins in talks involving congressional Democrats, Republican counterparts and the White House. The bipartisan negotiations around the payment stablecoins bill broke down on Thursday’s markup as Chair Patrick McHenry inculpated the White House for objecting to some provisions and not showing urgency.

The partisan clash also involved committee Democrats led by the agency’s ranking member Maxine Waters and Stephen Lynch, who faulted the Republicans for lacking patience and railroading parties involved in the process. Nonetheless, the version of the stablecoin bill eventually settled upon was approved by the committee in a vote concluding 34-16, which referred the bill to the House floor.

=> The debut of the blockchain-powered digital passport platform, Worldcoin, has stirred heated debates in the cryptocurrency community. Launched with support from major exchanges like Binance, Worldcoin relies on iris scans through specialized Orb hardware for "proof-of-personhood."

While some laud its potential for universal basic income distribution, critics, including Ethereum's Vitalik Buterin, express concerns about privacy, security, and centralization. Twitter's Jack Dorsey finds the project's "global scale alignment" attempt amusing. Anita Posch warns of data management risks. As the community remains divided, Worldcoin faces challenges to prove its worth amidst skepticism and criticism.

=> Russia has signed the digital ruble bill into law, which will take effect on August 1, 2023. The digital ruble is designed to serve as a payment and money transfer method and will act as the third form of money alongside cash and non-cash rubles.

However, Russian citizens will not be forced to use the central bank's digital currency (CBDC), and the use of the digital ruble will be a voluntary choice left up to individuals to decide. The government doesn't expect mass adoption of the digital ruble in Russia before 2025 or even 2027.

Curve Finance exploit

On July 30, Curve Finance, a prominent stablecoin lending protocol, experienced a significant exploit on several stable pools. The exploit was traced back to vulnerabilities in specific versions of the Vyper compiler, a smart contract programming language for the Ethereum Virtual Machine (EVM).

The exploit mechanism, known as “malfunctioning reentrancy locks,” allowed the attacker to bypass the intended safeguards and drain funds from the targeted contracts. According to Curve Finance CEO Michael Egorov in a Telegram channel, the swap pool has been drained of 32 million CRV tokens, which are worth over $22 million. However, experts estimate that the total loss could be more than $40 million.

The exploit significantly impacted the DeFi ecosystem, with several projects reporting substantial financial losses. These include decentralized exchange Ellipsis, Alchemix’s alETH-ETH pool, JPEGd’s pETH-ETH pool, and Metronome’s sETH-ETH pool. The total losses were estimated to be upwards of $24 million. The incident triggered a wave of panic across the DeFi ecosystem, prompting a flurry of transactions across various pools.

Curve Finance’s total value locked has decreased by 43% since the exploit, dropping from $3.26 billion to $1.87 billion, CRV token is down by 12%. Surprisingly, CRV DAO perpetual futures are still trading at a small premium, indicating that traders are more focused on moving positions away from the DEX (regarding total value locked) rather than shorting the token

The incident underscores the importance of robust security measures in DeFi protocols. As the investigation progresses and more updates unfold concerning the hack, developers are expected to work closely with the Vyper team to address the vulnerabilities and prevent future exploits. The market seems to have digested this exploit, however, the exact scope of this vulnerability and its implications on the broader DeFi ecosystem is yet to be fully assessed.

Cryptos: spot, derivatives and “on chain” metrics

The crypto market closes July on a visible downtrend following another disappointing week. As the SEC vs. crypto war continues, most assets have performed poorly for the second week in a row. Firstly, the Commission maintains its crackdown approach towards digital assets. On the other hand, the US politicians criticized it for being too rough on a yet emerging financial sector. This back-and-forth led to an underwhelming performance across the board. Fortunately, the market capitalization decreased by only around $10 billion.

Bitcoin and Ether prices dropped during this last weekend, but remained above the support levels of US$29,000 and US$1,800 respectively. The drop coincided with news of a hack at DeFi exchange Curve Finance. Most other top 10 non-stablecoin cryptocurrencies traded lower, with Tron’s TRX token leading the losers

Gainers / Losers last 7 days, block size volume.

Bitcoin

That back and forth movement had left a minor operating event of weakness within this minor value area that we have been generating since late June. We believe it will most likely resolve as distributive with targets at the high volume node below $28100.

As we said last week, as long as the price remains above the high volume node of $28100 and the Vwap anchored to the previous local highs, the long scenario should be maintained. However, it is vital for the bulls to regain the upper volume node of $30,250 in order to be able to continue to raise bullish scenarios.

Bitcoin 24/07/23 30 min chart

Bitcoin 31/07/23 30 min chart

Moving up the timeframe, the scenario of effective bullish imbalance of the entire lower value area is still on the table. The verticality of the rise leaving a somewhat inefficient auction and the clash with the third typical deviation of the main Wwap are the only impediments to further upside for the time being. The market must hold the $28100 level and remain above the Vwap anchored at the previous local highs, losing this zone would put an end to any bullish continuation scenario.

Bitcoin 24/07/23 4h chart

Bitcoin 31/07/23 4h chart

Bitcoin’s 30-day correlation coefficient with the Nasdaq composite sits at -0.03, and its equivalent with the S&P 500 sits at -0.07, meaning that in both cases, BTC’s price holds a very slight negative correlation with shares (a break from the high positive correlation during COVID-era spending, especially to tech stocks).

Despite the recent rally, market depth has failed to recover since the FTX collapse.

Binance's spot market share dropped to 50% from 64% earlier this year. Coinbase also experienced a decline, while smaller exchanges gained ground.

Glassnode’s weekly on-chain report focuses on BTC “whale” activities. Glassnode notes that whales (entities with a minimum of 1K BTC) “appear to be increasingly active in recent months” with 41% of total BTC inflows to exchanges in recent weeks coming from whales, and 82% of this has been to Binance specifically. Most of these whale depositors are Short-Term Holders (STH, meaning their BTC are held for fewer than 5 months).

Glassnode’s Trend Accumulation Score by Cohort shows that most small entities with less than 100 BTC have slowed their spending over the past month. On the other hand, the subset of whales holding more than 1,000 BTC exhibited divergent behavior, with those holding more than 10,000 BTC distributing and those holding 1,000 to 10,000 BTC accumulating at a much higher rate.

This behavior suggests that whales are actively shuffling their holdings, moving funds internally between institutions.

Isolating coins flowing between Whale entities and exchanges shows that the aggregate Whale balance has declined by 255k BTC since 30 May. This is the largest monthly balance decline in history, hitting -148k BTC/month. This indicates that there are noteworthy shifts happening within the Bitcoin Whale cohort.

Short-Term Holder Dominance across Exchange Inflows has exploded to 82%, which is now drastically above the long-term range over the last five years (typically 55% to 65%). From this, we can establish a case that much of the recent trading activity is driven by Whales active within the 2023 market (and thus classified as STHs).

Ethereum

No relevant changes for Ethereum that continues to resist breaking the Vwap anchored at all time highs. We need to see a real change of character, breaking this level in a strong way to build solid and consistent long scenarios. Any loss of buying response in the $1700 - $1500 area would set off all alarms.

Ethereum 24/07/23 4h chart

Ethereum 31/07/23 4h chart

BNB

We will closely monitor the evolution of BNB as a measure of risk perception. BNB is the cryptocurrency coin that powers the BNB Chain ecosystem. BNB is one of the world's most popular utility tokens and it is used primarily to pay transaction and trading fees on the Binance exchange. It is Binance's flagship token.

At first glance we note that the Vwap anchored at highs has never been exceeded or practically tested since late 2021. The vigorousness with which the Vwap anchored at the local lows of June 2022 has been broken through makes us aware of the major weakness on this token.

Clearly the area to watch is the historical support at $220, from there Binance could be in serious trouble.

BNB 24/07/23 4h chart

BNB 31/07/23 4h chart

Classic markets

The SP500 posted its third positive weekly result in a row, gaining around 1%, and the Nasdaq added about 2%. The Dow on Wednesday climbed for the 13th trading day in a row, marking that index’s longest positive streak since 1987. On the heels of the U.S. Federal Reserve’s latest interest-rate increase, the yield of the 10-year U.S. Treasury bond closed above 4.00% on Thursday for the fourth time this year. The yield pulled back slightly on Friday, when it was trading around 3.97%, well above the previous week’s closing level of 3.85%.

The growing divergence between two long duration assets, TLT (20-30 year US Treasury bond ETF) and QQQ (NASDAQ 100 market cap-weighted ETF) is worth watching.

Similarly, the divergence between the SP500 and net Fed liquidity is broadening, suggesting that the markets may be running a bit hot. A surge of liquidity combined with share buybacks and multiple expansion were key drivers of the rally up until recently.

Zooming out we can see this divergence in the S&P 500 vs the 30-year Treasury total return, with the largest divergence of this kind since the Dot Com bubble. This could illustrate a growing risk of a re-rating downward for risk assets of long duration US debt doesn’t recover significantly.

The S&P 500 equity risk premium hit the lowest level in two decades, which will be a headwind for longer-term returns.

Crowding in forward Growth factor is now at 97%ile, nearing levels last seen during the TMT bubble. JP Morgan

Meme Index has been outperforming SP500 for third consecutive month, with July being strongest (thus far) since this past January.

There’s palpable excitement in the options market, as equity call volumes are surging, and we see single stock skew becoming more and more lopsided towards calls as upside bets are placed. Suggesting most of this call volume is bought to open.

BofA notes that longer-term SPX puts have not been this cheap in modern times: "It has never cost less to protect against an S&P decline over the next 12 months." The 1-year SPX 95-75% SPX PUT SPREAD 95-75% offers a maximum return of about 8x.

Looking at the S&P 500, forward 12-month EPS seems to be lagging the trajectory of the index itself, which along with valuations, suggest that stocks may be expensive here.

Though the most overvalued stocks are the so-called magnificent seven. Netting them out of the index leaves us with a forward P/E of 16.6. Not terribly expensive in comparison, but we are also seeing earnings down over 7% in Q2 so far for the S&P 500, suggesting that we're in the third quarter of an earnings recession.

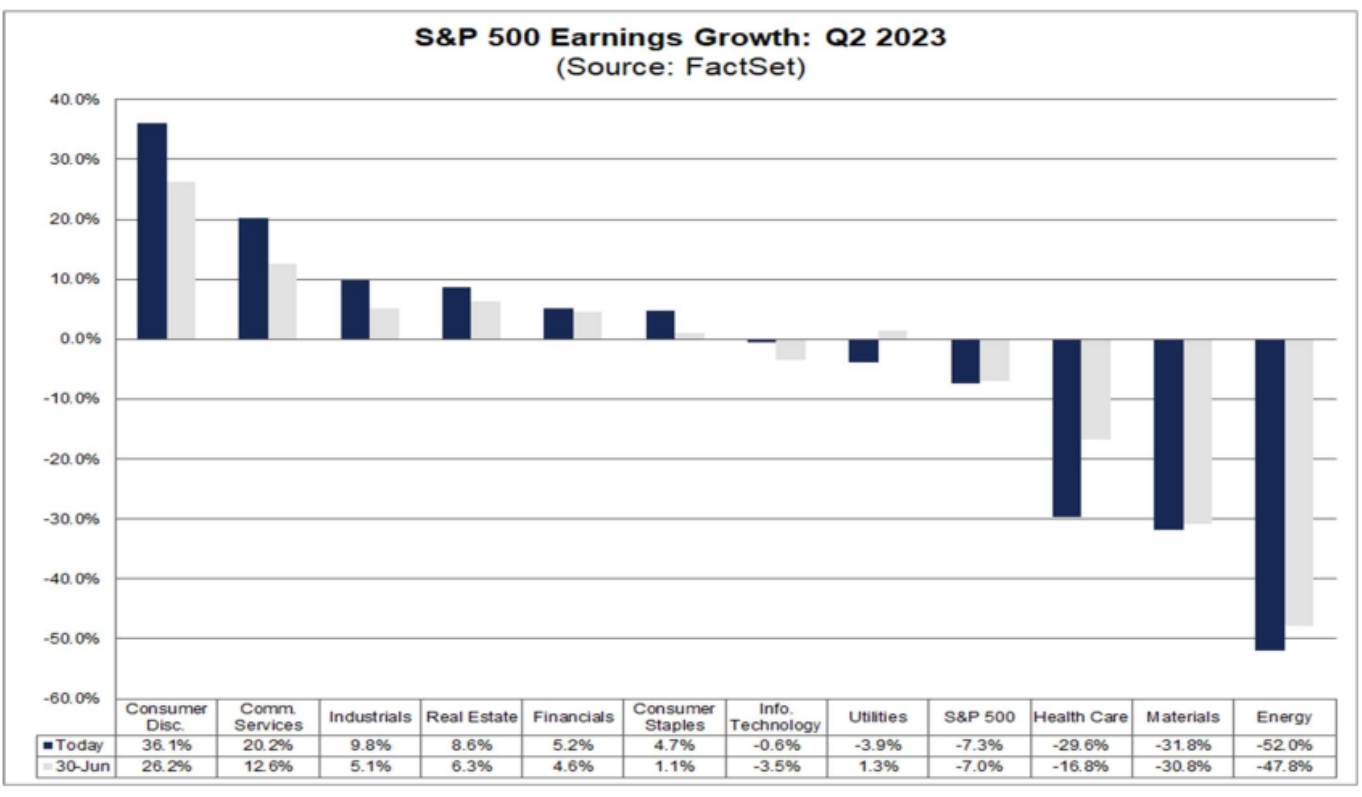

Positive earnings surprises have been a key theme so far, with consumer discretionary, info tech, communications, and industrials leading.

Consumer discretionaries, communications, industrials, and real estate leading the way for EPS growth in Q2. On the other side, energy, materials, and health care are showing strong negative earnings growth.

Systematic equity positioning is in the 72th percentile and discretionary equity positioning is in the 86th percentile.

BOFA CTAs model:

The market managed to recover the Vwap anchored at previous highs, opening the door to further rallies within an atypically low volatility for a Fed Meeting. It was not until the news from the Bank of Japan that volatility appeared and severely so. The VIX experienced the second most powerful intraday spike of the year. The market went through this entire value area, in a clear sign of weakness and seller control. However, that show of weakness was again ignored by the market thanks to the invaluable help of ODTE options and risk-averse participants who see every unique opportunity to jump on the ride.

The key this week is the final achievement of this structure, re-accumulation or distribution? The key as always will be in the positioning of options and the evolution of gamma exposure. We will be keeping a close eye on various volatility metrics, with special attention to the SVIX (short VIX ETF). Following the Bank of Japan's announcement, a truly massive sell off began, indicating a risk off not seen for weeks. Clearly the market is very afraid of everything that can alter its status quo and its way of functioning and this always comes from the hand of the Central Banks. On Friday, at the close of the week, the SVIX picked up demand, largely canceling out the sell-off experienced the previous day.

The Bulls this week should keep the market from moving back inside the value area, in turn moving the market away from the zero gamma level. Any re-entry into the range could again give life to a distributive scenario.

24/07/23 SP500 futures small picture

31/07/23 SP500 futures small picture

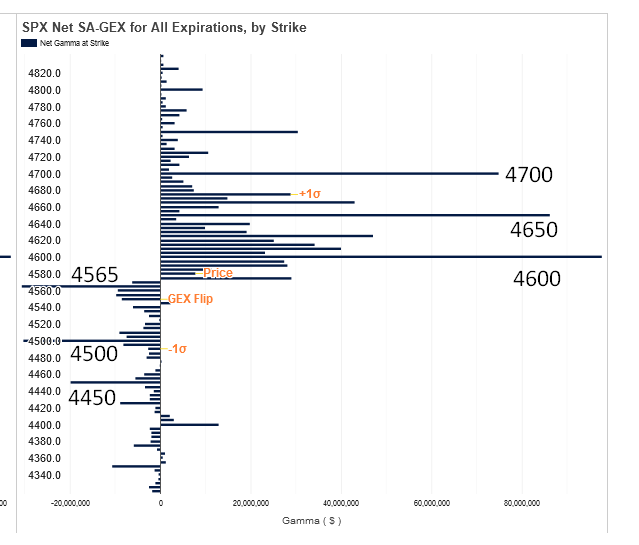

The huge Gamma now sitting at the 4600 strike which is "not a puncher" and keeps us "stuck" around here, despite having exited the Op-Ex. Significant open interest generation is observed in the upper strikes, 4650 and 4700, although since last week bearish and hedging flows have been observed on the puts side.

The key for this week from a gamma point of view, is for the market to break 4600 or be rejected. Conquering the gamma stack, converting the 4600 into support would open the door to further rises. The market insists on the long side, however the zero gamma level is progressively approaching the trading zone with the risks that this entails. Currently the flip point is at 4452.5 points.

Gamma Profile 24/07/23

Gamma Profile 31/07/23