.png)

.png)

Summary

The major U.S. equity benchmarks started August with a down week after closing out a strong July. Stocks declined amid rising Treasury yields and an unexpected downgrade to the U.S. government’s credit rating. The technology-heavy Nasdaq Composite suffered the largest losses for the week.

Credit ratings become relevant again when Fitch downgraded the US, even if US Treasury Secretary Janet Yellen thinks they are “outdated”. The surprise move may mean that investors will keep a closer eye on upcoming credit ratings, with Germany and Switzerland’s due for a review next week. We also have key inflation data for the US and China. Markets essentially want to see core CPI in the US fall harder and faster to justify their bets that the Fed is done hiking rates. And we’ll also find out if China’s annual inflation rate falls below zero for the first time in over two years.

In a busy week for corporate earnings releases, investors were especially focused on results from mega-cap names Amazon and Apple, which reported earnings after markets closed on Thursday. Amazon significantly beat expectations, helped by strength in its core retail business, and the company’s stock rallied more than 9% at Friday’s open. Apple, meanwhile, traded down about 3% after a mixed report that showed strength in its services business, although iPhone sales disappointed.

Bitcoin (BTC), the oldest and still the most relevant cryptocurrency in the world, failed to cross the $30,000 threshold over the past week, lending a gloomy outlook to the overall crypto market. The global market cap remained at $1.16 trillion, failing to show any signs of a bull streak. While the overall market sentiment remains neutral, it can be expected that the market might continue trading sideways, unless a major pro-crypto development occurs.

Whitehats hackers and attackers have returned over 73% of all funds stolen from Curve Finance after its early August exploit. The platform lost over $73 million worth of various tokens, causing contagion effects in the broader ecosystem. The relatively swift recovery has bolstered sentiment for CRV tokens, which have pared most of the losses from a 30% drop following the attack.

Shortly following the attacks, Curve offered a 10% bounty to attackers for the return of the funds. On Friday, the attacker started to return funds to Alchemix after confirming the deposit address in a blockchain message. Over $18 million in stolen funds are still remaining, with Curve opening up the bounty to the public on Sunday night.

CRV lost almost 30% of value, from 72 cents to as low as 50 cents, in the days following the exploit and has since pared losses amid positive developments, trading at 61 cents as of Monday morning. Curve Finance and CEO Michael Egorov have received support from prominent names in the crypto space, including Justin Sun. Sun’s CRV purchase comes amid worries that liquidating Egorov’s $100 million loans would trigger an implosion of the DeFi ecosystem.

Macro y news

Earnings for this coming week:

U.S Macro data

August started with a bang, as the market's summer calm was disrupted by news that Fitch, one of the "Big Three" credit agencies, downgraded the U.S. debt rating from AAA to AA+. This is the second credit downgrade in U.S. history after a similar decision by Standard & Poor's in August of 2011. U.S. political brinkmanship and debt concerns are not new, but the Fitch downgrade shines the spotlight on the worsening fiscal outlook.

When the U.S. lost its AAA rating from Standard & Poor's more than a decade ago, a decision that has not yet reversed, it triggered a 4.8% decline in the S&P 500 the day of the announcement on August 4 and another 6.5% decline on August 81. Stocks remained volatile over the following two months. But counterintuitively, investors gravitated toward government bonds and the U.S. dollar as safe havens against the uncertain backdrop.

As reasons for the downgrade, Fitch cited fiscal deterioration, a high and growing government debt burden, and eroded fiscal confidence stemming from repeated debt-limit standoffs. After this year's aggressive Fed rate hikes to tame inflation, interest costs are rising fast and becoming a larger burden to the budget. Though at around 2% currently, interest payments on federal debt as a percent of U.S. GDP are well below those observed in the 1980s and 1990s.

US state and local governments just experienced the worst decline in income tax revenues ever recorded. This was the second steepest year-over-year percentage decline in history, with only the GFC having a worse outcome. Note that Federal tax receipts are also dropped again, now at recessionary levels and approaching -10% on a YoY basis. This is a clear indication of the continued fundamental deterioration of the economy, which sharply contrasts with overall financial assets that remain at excessively inflated valuations.

US Deficit = 8.5% (% of GDP)

Unemployment rate = 3.6%

Prior to COVID, the US had never run a deficit that was >5% of GDP when UE was <4%.

Job security and income gains have been a key pillar of support behind this year's resilient economy. However, the tight labor market and strong wage growth have also been a source of concern for the Fed as it aims to bring inflation back to its target. From the lens of the Fed, the July employment data provided mixed takeaways.

The Job Openings and Labor Turnover Survey from the Bureau of Labor Statistics showed a modest drop in the number of job openings in June, although layoffs declined for a third straight month. ADP’s private employment survey was better than expected but did show hiring eased to 324,000 from 455,000 in June.

225k Jobs out of the total 324k jobs added were hospitality and leisure jobs, manufacturing lost almost 40k jobs.

The Labor Department’s closely watched monthly nonfarm payroll report showed that employers added 187,000 jobs in July, about the same as June’s downwardly revised 185,000. The past two months’ data, while still showing health in the labor market, point to a notable slowing from the first five months of the year when the economy added an average of 287,000 jobs a month. The unemployment rate ticked down to 3.5% from 3.6% the prior month, while wages grew 4.4% over the 12-month period, unchanged from June.

The Institute for Supply Management manufacturing Purchasing Managers’ Index came in at 46.4, a bit lower than the 46.9 consensus and the ninth straight month under 50, the level that indicates contraction. The last 3 times ISM Manufacturing was this low, the US economy was in or about to be in a recession. You have to go back to 1995-96 to find a lower reading with no recession.

US service sector activity expanded at a more moderate pace in July, restrained in part by a softening of employment growth. The Institute for Supply Management’s services index decreased 1.2 points to 52.7 last month.

Eurozone macro data

Annual inflation in the euro area slowed further to 5.3% in July from 5.5% in June but remained well above the European Central Bank’s 2% target. Inflation also declined in Germany and France, the bloc’s two largest economies.

Eurozone Jul. Core CPI (YoY): 5.5%, [Est. 5.4%, Prev. 5.5%]

Eurozone Jul. CPI (MoM): -0.1%, [Est. -0.1%, Prev. 0.3%]

Eurozone Jul. CPI (YoY): 5.3%, [Est. 5.3%, Prev. 5.5%]

Eurozone Q2 GDP (QoQ): 0.3%, [Est. 0.2%, Prev. 0.0%]

Eurozone Q2 GDP (YoY): 0.6%, [Est. 0.5%, Prev. 1.1%]

The eurozone economy expanded 0.3% sequentially in the second quarter, after gross domestic product (GDP) shrank or stagnated in the previous two quarters. Germany’s GDP was unchanged, while Italy’s economy contracted by 0.3%.

Forward-looking purchasing managers’ surveys indicated a weaker start to the third quarter. The final reading of the composite index of business activity in services and manufacturing was revised slightly lower to 48.6 in July. For this indicator, readings below 50 signal contraction.

Germany

Factory orders m/m +7% exp. -2%; prior 6.2%

Factory orders WDA y/y +3% exp. -5.3%; prior -4.4%

Germany June industrial production falls 1.5% m/m; est. -0.5%

Germany June industrial production falls 1.7% y/y; est. -0.2%

Swiss manufacturing activity plummeted at the start of the third quarter. While the gauge has been below the vital threshold of 50 which separates growth from contraction since the start of the year, this is the worst reading since 2009.

UK macro data

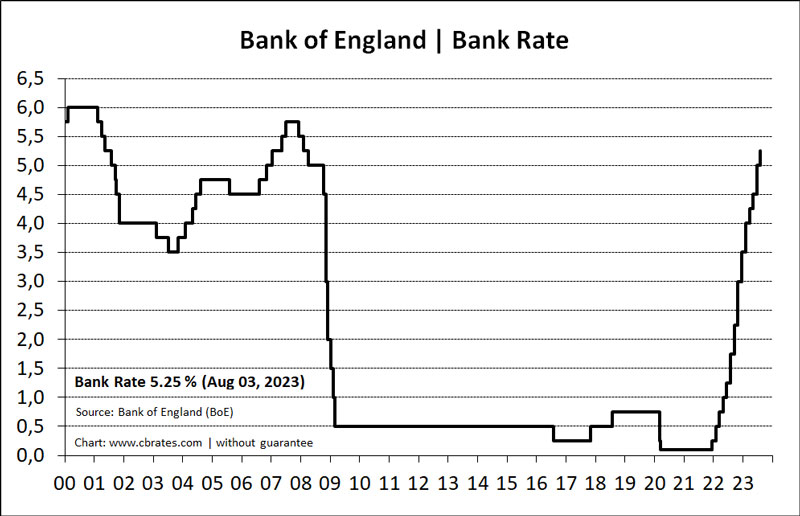

The BoE raised its key interest rate by a quarter of a percentage point to a 15-year high of 5.25%. It warned that rates were likely to stay high for some time, saying the MPC (Monetary Policy Committee) will ensure that Bank Rate is sufficiently restrictive for sufficiently long to return inflation to the 2% target.

The central bank predicted the inflation rate would fall to 4.9% by the end of this year, a faster pace than in its May forecast. BoE estimates for economic growth were little changed at 0.5% this year and next.

The UK housing market remained weak amid the highest mortgage rates since 2008. House prices fell 3.8% year over year in July, worse than June’s drop of 3.5% and the fastest decline since July 2009, according to a closely watched index published by the Nationwide Building Society.

BoE mortgage data for the second quarter showed the first quarterly decline in the value of net mortgage lending since records began in 1987.

Bankruptcies in England and Wales are close to their Great Financial Crisis peak.

Japan macro data

Following its July 28-29 monetary policy meeting, the BoJ decided to keep its key short-term interest rate unchanged at -0.1% and that of 10-year JGB yields around zero percent. It judged that a sustainable and stable achievement of its 2% price stability target had not yet come in sight.

However, the central bank surprised investors with the announcement that it would conduct YCC with greater flexibility to enhance the sustainability of monetary easing under the current framework. While it will continue to allow 10-year JGB yields to fluctuate in a range of around plus and minus 0.5% from the zero percent target level, greater flexibility means that it will regard the upper and lower bounds of the range as references, not as rigid limits, in its market operations. The BoJ will also offer to buy 10-year JGBs at 1.0% (changed from 0.5%) every business day through fixed rate purchase operations.

The yield on the 10-year Japanese government bond (JGB) rose to 0.65%, around a nine year high, from 0.55% at the end of the previous week. This followed the Bank of Japan’s (BoJ’s) July monetary policy tweak to effectively allow interest rates to rise more freely, by increasing the flexibility around its yield curve control target, as well as its offer to buy 10-year JGBs at 1.0% (up from 0.5%) each day.

During the week, the BoJ announced two unscheduled bond-purchase operations, aimed at slowing the speed of yield gains. BoJ Governor Kazuo Ueda has said that under current circumstances, he does not expect yields to rise to 1%. Given the BoJ’s continued commitment to its accommodative stance and Japan’s wide interest rate differential with the U.S., the yen weakened to about JPY 142.6 against the U.S. dollar, from around 141.1 the prior week. Speculation was ongoing that Japan’s Ministry of Finance could intervene in the foreign exchange markets to shore up the yen’s value.

Japan’s services sector expansion slowed in July, according to the latest Purchasing Managers’ Index (PMI) data compiled by au Jibun Bank. The headline services index fell to 53.8 in July, from 54.0 in June. The manufacturing PMI slipped further into contraction territory, to 49.6 in July from 49.8 the prior month. Both output and new orders fell modestly, due primarily to weak demand for manufactured goods in both domestic and international markets.

China macro data

China's cabinet, the State Council, announced new measures to revive consumption. The wide-ranging policies focused on removing restrictions on consumption in sectors including autos, real estate, and services, Reuters reported. Local regions were also encouraged to provide subsidies for home appliance purchases and home renovation materials in rural areas. However, the measures contained no mention of direct cash support to consumers to bolster spending, which some analysts have called for.

The People’s Bank of China (PBOC) pledged to support the development of China's real estate market during its biannual work conference. The PBOC said it would continue to reduce housing loan interest rates and down payment ratios and guide commercial lenders to adjust rates on existing mortgages. The PBOC’s pronouncements raised speculation that the central bank may cut the reserve requirement ratio for domestic lenders in the near term as the government ratchets up efforts to bolster China’s flagging recovery.

China’s official manufacturing Purchasing Managers’ Index (PMI) rose to 49.3 in July as expected, from June’s 49. However, it stayed below the 50-point threshold separating growth from contraction for the fourth consecutive month. The nonmanufacturing PMI declined to a weaker-than-expected 51.5 from 53.2 in June.

The private Caixin/S&P Global survey of manufacturing activity eased to a below forecast 49.2 in July from June’s 50.5 and marked a return to contraction after expanding for two months.

Both Manufacturing China PMI indices ('official' and Caixin) are now below 50, signaling the Chinese economy continues to deteriorate, especially now that the Services PMIs are heading toward 50.

Bonus macro data: credit crunch and macro slowdown

While stock market FOMO has magnetized crowds, default rates have started to mount in corporate bonds and leveraged loans. That is, pressures in the credit markets are likely to deepen and spread, which feeds on its interactive loop with the economy.

Cash-strapped U.S. trucking company Yellow has ceased operations and is filing for bankruptcy after failing to reorganize and refinance over a billion dollars in debt. The company was the third-biggest U.S. trucker specializing in the less than truckload segment that combines shipments from different customers in the same trailer.Its customers included large retailers like Walmart and Home Depot, manufacturers and Uber Freight, some of which paused cargo shipments to the company for fear those goods could be lost or stranded if the carrier went bankrupt.

Shipping giant Maersk warns of a sharp slowdown in global trade as it reports profit plunge. The world’s second largest shipping company, often seen as a bellwether for global trade, posted a second-quarter profit before interest, tax, depreciation and amortization (EBITDA) of $2.91 billion. This was well below the record $10.3 billion for the same quarter in 2022.

Maersk warned of a deeper pullback in global shipping container demand, and now expects volumes to fall by as much as 4% versus a previous worst case scenario of 2.5% as companies cut their inventories amid recession risks in Europe and the U.S.

Crypto News

July saw the worst crypto plunge of the year, with a $486 million loss due in part to a major exploit by Multichain. However, there is some good news: the mastermind behind the $61 million Curve Finance attack has returned $8.9 million and conventional institutions continue to demonstrate interest in this space. This time, financial service providers Direxion and ProShares filed to launch exchange-traded funds that would hold futures contracts involving BTC and ETH.

=> At least 11 firms have filed with the SEC to launch Ethereum futures-based ETFs, in a rush that echoes the Bitcoin ETF fervor. The Volatility Shares Ether Strategy ETF, which is known for its 2x Bitcoin Strategy ETF, led the effort by submitting its own on July 28.

Others followed: Bitwise Ethereum Strategy ETF, VanEck Ethereum Strategy ETF, Roundhill Ether Strategy ETF, ProShares Short Ether Strategy ETF, ProShares Ether Strategy ETF, and the awaited Grayscale Ethereum Futures ETF. The SEC has not yet approved Ethereum futures ETFs, but change is on the horizon. Approval would see ETFs live 75 days post-filing, starting with Volatility Shares on October 12.

=> The U.S. Securities and Exchange Commission (SEC) has filed legal action against Richard Schueler, aka Richard Heart, alleging unregistered issuance of three tokens. According to the complaint, filed in a New York court on July 31, Heart amassed over $1 billion through unregistered sales of crypto securities, including Hex, PulseChain (PLS), and PulseX (PSLX).

Heart, accused of violating federal securities laws and defrauding global investors, reportedly promised extravagant wealth. Meanwhile, the SEC claims he diverted $12.1 million for personal purchases, like a 555-carat diamond and luxury cars.

=> The CEO of Binance, CZ, has issued an urgent alert regarding a surging crypto scam in which fraudsters mimic wallet addresses to divert transactions, exploiting users. This technique involves crafting addresses resembling the victim's and executing 'dust transactions' to imprint them in transaction history. If victims duplicate these, funds go to scammers.

=> Prominent lawmakers have urged the Biden administration to initiate a crackdown on crypto tax evaders and enforce tax reporting guidelines for users in the crypto space. In a nightmare scenario, a report has claimed that DoJ officials are contemplating bringing fraud charges against Binance, the world’s largest cryptocurrency exchange.

=> In light of the evolving regulatory landscape surrounding digital currencies in the US, Revolut has decided to shut down its crypto offerings in the country.

=> Bankrupt crypto platform, Voyager Digital Holdings Inc., may have been a victim of a hacking attack during the court-supervised process of liquidating assets to repay its customers.

=> Cryptocurrency's volatile market reached a low point in July when a DeFi report revealed a staggering $486 million loss, six times the previous year's figure. The Multichain exploit accounted for nearly half the losses, draining $231 million.

Meanwhile, amid high-profile breaches, recovery efforts fell drastically short, reclaiming only $6.15 million of the $486.35 million lost. Ethereum suffered the most, losing $447 million across 36 cases, while access control issues contributed a majority of the $364 million losses.

=> Justin Sun, the founder of Tron, acquired 5 million CRV tokens from Curve’s Michael Egorov in a likely over-the-counter (OTC) deal for US$2.9 million, which is lower than the market price. Alongside the acquisition, Sun announced a partnership between Tron and Curve to introduce a stUSDT pool, aiming to empower the community and enhance decentralized finance. The CRV market has faced turbulence, hitting a low point at US$0.50 before rebounding to US$0.59, and Egorov attempted to stabilize his DeFi position amid sharp volatility

=> In an unexpected turn of events, the hacker behind the $61.7 million Curve Finance attack is returning $8.9 million to the Alchemix and Curve teams. The attacker, who took advantage of a reentrancy bug, has begun a partial refund, citing a desire to preserve the integrity of the exploited protocols.

=> The US Securities and Exchange Commission has implemented new rules for public companies, requiring them to disclose cyberattacks promptly. Other DeFi protocols, like BNB Smart Chain, have also experienced copycat attacks due to the Vyper vulnerability, with approximately US$73,000 stolen across three exploits.

Curve Finance exploit

On July 30, Curve Finance, a prominent stablecoin lending protocol, experienced a significant exploit on several stable pools. The exploit was traced back to vulnerabilities in specific versions of the Vyper compiler, a smart contract programming language for the Ethereum Virtual Machine (EVM).

The exploit mechanism, known as “malfunctioning reentrancy locks,” allowed the attacker to bypass the intended safeguards and drain funds from the targeted contracts. According to Curve Finance CEO Michael Egorov in a Telegram channel, the swap pool has been drained of 32 million CRV tokens, which are worth over $22 million. However, experts estimate that the total loss could be more than $40 million.

The exploit significantly impacted the DeFi ecosystem, with several projects reporting substantial financial losses. These include decentralized exchange Ellipsis, Alchemix’s alETH-ETH pool, JPEGd’s pETH-ETH pool, and Metronome’s sETH-ETH pool. The total losses were estimated to be upwards of $24 million. The incident triggered a wave of panic across the DeFi ecosystem, prompting a flurry of transactions across various pools.

Curve Finance’s total value locked has decreased by 43% since the exploit, dropping from $3.26 billion to $1.87 billion, CRV token is down by 12%. Surprisingly, CRV DAO perpetual futures are still trading at a small premium, indicating that traders are more focused on moving positions away from the DEX (regarding total value locked) rather than shorting the token

The incident underscores the importance of robust security measures in DeFi protocols. As the investigation progresses and more updates unfold concerning the hack, developers are expected to work closely with the Vyper team to address the vulnerabilities and prevent future exploits. The market seems to have digested this exploit, however, the exact scope of this vulnerability and its implications on the broader DeFi ecosystem is yet to be fully assessed.

Update

=> Decentralized finance (DeFi) protocol Curve Finance is extending a bug bounty offer to anyone who is able to identify the exploiter responsible for draining over $61 million from its pools on July 30. Curve and other protocols affected by the attack offered a 10% bug bounty to the hacker on Aug. 3, totaling more than $6 million. Upon accepting the offer, the hacker returned stolen assets to Alchemix and JPEGd, but did not complete refunds to other affected pools. As the deadline has passed, anyone who can identify the attacker will now be rewarded with assets worth $1.85 million.

Prior to returning the funds, the attacker posted a message that appears to have been directed at the Alchemix and Curve teams, claiming to be willing to return the funds only because they didn’t want to “ruin” the projects involved. “I’m refunding not because you can find me, it’s because I don’t want to ruin your project,” reads the on-chain message.

=> DeFi platforms Curve Finance, Alchemix, and Metronome have announced a joint initiative to recover the stolen funds in the wake of the recent exploits that hit Curve’s pools.

=> Curve Finance and CEO Michael Egorov have received support from prominent names in the crypto space, including Justin Sun and DCF God.

Justin Sun, the founder of the Tron blockchain, has purchased five million Curve tokens (CRV) from an address labeled “Curve.fi Founder” in an attempt to help with the decentralized exchange Curve Finance’s bad debt situation.

As disclosed by blockchain analytics platform Lookonchain, Sun bought the tokens at an average price of $0.4 via an over-the-counter transaction, amounting to $2 million, which he paid in Tether (USDT). The Tron founder acquired the assets below their current trading price of $0.59.

Sun’s CRV purchase comes amid worries that liquidating Egorov’s $100 million loans would trigger an implosion of the DeFi ecosystem. The concerns were heightened after Curve Finance suffered an exploit that led to the loss of more than $47 million.

According to crypto research firm Delphi Digital, the loans are backed by 47% of all CRV in circulation, amounting to 427.5 million tokens. Egorov borrowed 63.2 million USDT on Aave and pledged $305 million worth of CRV as collateral. He supplied another 59 million CRV against 15.8 million FRAX debt on Frax Finance. Egorov’s loan on Aave has a liquidation threshold of 55%, meaning his position can be liquidated if CRV falls to $0.37. Although his Frax debt is much less than the Aave position, Delphi Digital noted that the former is riskier because of its time-weighted variable interest rate.

Cryptos: spot, derivatives and “on chain” metrics

The crypto market ends a largely disappointing week with very few things to celebrate. Most assets have lost substantial gains, with some recording double-digit losses. Most cryptocurrencies have reverted to pre-summer values and are looking at an uphill mid-Q3 battle.

The king of cryptocurrencies has spent another week below the $30,000 level. Moreover, it seems to have lost the necessary drive to overcome the market’s volatility and climb above $30,000. Ethereum is also down trending, struggling for weeks to climb above $2,000. Almost all altcoins are trading in the red for the week, with very few exceptions. The DeFi sector lost nearly $2.5 billion to the total value in locked protocols (TVL), now at $45.44 billion.

Gainers / Losers last 7 days, block size volume.

Bitcoin

As we said last week, as long as the price remains above the high volume node of $28100 and the Vwap anchored to the previous local highs, the long scenario should be maintained. However, it is vital for the bulls to regain the upper volume node of $30,250 in order to be able to continue to raise bullish scenarios.

Bitcoin 31/07/23 30 min chart

Bitcoin 07/08/23 30 min chart

Moving up the timeframe, the scenario of effective bullish imbalance of the entire lower value area is still on the table. The verticality of the rise leaving a somewhat inefficient auction and the clash with the third typical deviation of the main Wwap are the only impediments to further upside for the time being. The market must hold the $28100 level and remain above the Vwap anchored at the previous local highs, losing this zone would put an end to any bullish continuation scenario.

Bitcoin 31/07/23 4h chart

Bitcoin 07/08/23 4h chart

We can see that the volume traded of bitcoin has fallen even in the derivatives market, which would be in line with reduced liquidity.

Realized volatility for Bitcoin has collapsed to historical lows.Across 1-month to 1yr timeframes, this is the quietest we have seen the corn since after March 2020.Historically, such low volatility aligns with the post-bear-market hangover periods (re-accumulation phase).

New All-time-high for #Bitcoin Long-Term Holder supply 🔵, now at 14.59M BTC (75% of circulating).

Bitcoin dropped from $32,000 to $29,000 but the number of new BTC addresses steadily rose.

Options Implied volatility for Bitcoin is literally half of what it was in 2021-22.BTC options markets are pricing in IV of 24% to 52%, compared to 60% to 100%+ throughout the last cycle. A major volatility crush is underway.

Put/Call ratios are at, or near all-time lows. The majority of traders are long calls. This has pushed 25-delta skew to all-time-lows, which is not a bullish signal. Put options are the cheapest they have ever been, the market is not hedged and does not perceive risk?

Ethereum

No relevant changes for Ethereum that continues to resist breaking the Vwap anchored at all time highs. We need to see a real change of character, breaking this level in a strong way to build solid and consistent long scenarios. Any loss of buying response in the $1700 - $1500 area would set off all alarms.

Ethereum 31/07/23 4h chart

Ethereum 07/08/23 4h chart

BNB

We will closely monitor the evolution of BNB as a measure of risk perception. BNB is the cryptocurrency coin that powers the BNB Chain ecosystem. BNB is one of the world's most popular utility tokens and it is used primarily to pay transaction and trading fees on the Binance exchange. It is Binance's flagship token.

At first glance we note that the Vwap anchored at highs has never been exceeded or practically tested since late 2021. The vigorousness with which the Vwap anchored at the local lows of June 2022 has been broken through makes us aware of the major weakness on this token.

Clearly the area to watch is the historical support at $220, from there Binance could be in serious trouble.

BNB 31/07/23 4h chart

BNB 07/08/23 4h chart

Classic markets

It’s been an ugly week. No one saw the Fitch downgrade coming for the US. Fitch did warn us earlier in the year when the debt ceiling negotiations were going on but, the timing of the downgrade now is odd. That sparked a sell off in the market.

The pace of earnings slows down in the week ahead. So far, just under 80% of S&P 500 firms have beaten Q2 consensus EPS estimates, while only 59% of firms have beaten revenue expectations. That current percentage of revenue beats is the lowest level in three years.

Apple did not impress investors, as earnings showed revenue slipping for the third straight quarter. Though earnings did beat estimates.CEO Tim Cook stated that the company is looking at generative ML models to enhance existing products, something that we felt we may hear on the call. That mention of AI wasn’t, however, enough to offset concerns.The company has risen nearly 50% YTD, but lackluster growth and financial engineering through aggressive buybacks propping up earnings per share may have investors wondering whether the company’s next engine of real growth, services, may be enough to offset diminishing hardware sales.

Amazon, the tech giant impressed investors and analysts with better than expected AWS and ecommerce growth and improvements in profitability brought on my major cost cutting initiatives. AWS growth is slowing, though, up only 12% year-over-year. Down from a 16% year-over-year gain last quarter. We expect that Amazon cloud growth could continue to slow, but we don’t expect it to go negative this year. Overall, Amazon had a reasonably good quarter vs expectations, but it is clear that there are challenges that lay ahead in their cloud growth and further steps that can be taken to improve their bottom line.

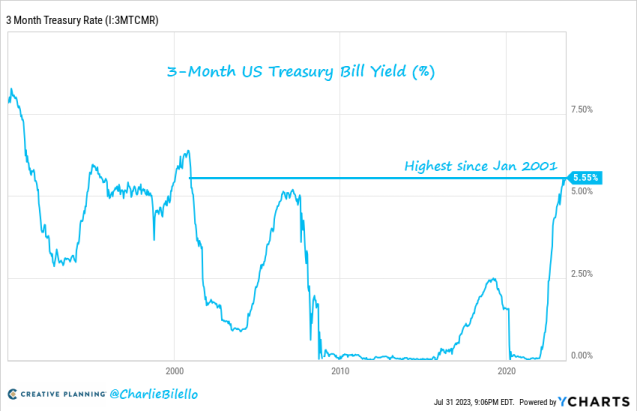

Wall Street retreated from a five consecutive month rally last week as spiking bond yields sent jitters to stock markets following Fitch’s US credit downgrade. At the same time, Friday’s job data shows that the US labor market slowed, securing another rate hike pause in September. Stocks experienced their first 1% down day since May, and the 10-year Treasury yield rose to a fresh high for the year, flirting with last year's cycle peak of 4.25%. The 3-Month Treasury Bill yield has moved up to 5.55%, its highest level since January 2001. A year ago it was at 2.41% and two years ago it was at 0.06%.

The implied intra-stock correlation is now very low relative to VIX. This implies that the market sees very little risk in the macro-outlook.

According to FINRA margin data, this is the largest 6-month increase in leverage on record. Leverage increased by ~$300B in the last 12 months.

CTAs overall allocation to equities was in the 86th percentile last week according Deutsche Bank.

GS CTA Models

Goldman: In the US, positioning is a headwind from here CTAs are almost at their max long position, with $43 billion in long positions in Eminis (a historical max of $50.2 billion). CFTC data shows that about half of the non-commercial short positioning in Eminis has been covered.

Over 1 week:

Flat tape: $21bn to sell (flat in S&P)

Up tape: $8bn to sell (-$1bn to SELL in S&P)

Down tape: $62bn to sell (-$6bn to SELL in S&P)

Over 1 month:

Flat tape: $37bn to sell (+$3bn to BUY in S&P)

Up tape: $1bn to sell (-$1bn to SELL in S&P)

Down tape: $283bn to sell (-$77bn to SELL in S&P)

Levels:

Short-term threshold = 4,444 (-1.3%)

Medium-term threshold = 4,260 (-5.3%)

Long-term threshold = 4,240 (-5.8%)

BOFA CTA Models

US stocks had their biggest one-day drop in months, joining a global sell-off, as a surprise downgrade of the country’s debt rating and stronger than expected jobs data raised concerns over the possibility of an extended period of higher interest rates that weigh on risky assets. This has led to profound changes in price dynamics and positioning in the options market.

Last week we mentioned: “The key this week is the final achievement of this structure, re-accumulation or distribution? The key as always will be in the positioning of options and the evolution of gamma exposure. We will be keeping a close eye on various volatility metrics, with special attention to the SVIX (short VIX ETF). Following the Bank of Japan's announcement, a truly massive sell off began, indicating a risk off not seen for weeks….The Bulls this week should keep the market from moving back inside the value area, in turn moving the market away from the zero gamma level. Any re-entry into the range could again give life to a distributive scenario”.

The upper value area has finally resolved as distributive with great speed, leaving even an effective bearish imbalance. Our bias is bearish with targets at the lows of the recent momentum (around 4400 points). Reversing the recent selling pressure is a complicated task for the Bulls. In our opinion as long as it remains below the upper VPOC (4580) and the Vwap (red) anchored at the most relevant previous lows the market is short.

31/07/23 SP500 futures small picture

07/08/23 SP500 futures small picture

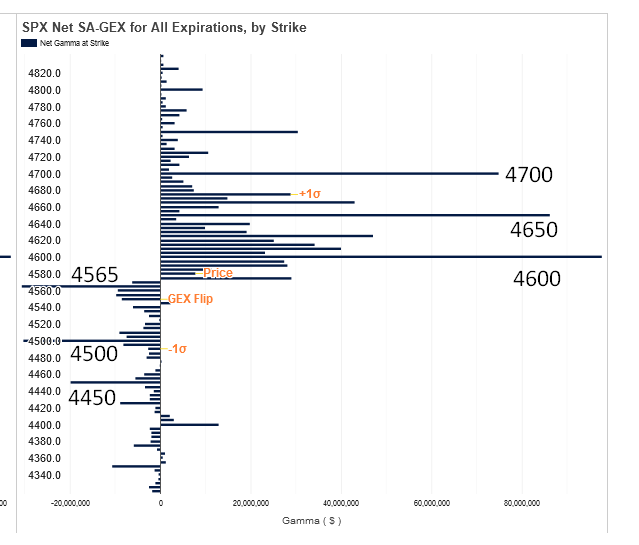

The change in gamma profile is dramatic. Call option walls remained stable, but some of the major put option walls moved downward; it is always interpreted as a bearish signal when key levels move downward. Now the strike with the highest gamma notional is 4400, observing also a large generation of open interest on the put side throughout the week. The market is already in a negative gamma regime, which translates into increased volatility. If the market fails to regain the 4500 point level for the 4400 strike to act as a powerful magnet for the market.

At the same time, 4400 points are considered an important zone for the positioning of the CTAs, which from this level onwards would proceed to massively unwind their long positioning.

Gamma Profile 31/07/23

Gamma Profile 07/08/23

If the market stays below the gamma flip point and the 4500 points the market will go for the 4400 points. Note how the SVIX (short VIX ETF) has already given several risk off warnings.